Trading 212 is one of the new zero fee free trading apps in the UK revolutionising how investors buy stocks and shares.

It has certainly changed our investing strategy with regard to how we buy shares – fees meant buying small amounts of a stock were far too costly before – now that’s simply not the case.

The cost of buying and selling shares has fallen over time, but remains sizeable on popular platforms Interactive Investor charging £8, AJ Bell £10 and Hargreaves Lansdown charging £12 per trade.

Also, we have a sweet Trading 212 bonus offer where you’ll be gifted a free stock to the value of £100 that you can snap up if you sign up through our link on the offers page here.

YouTube Video > > >

Ben has been using the app for the last several weeks and loves it – he’s set up an ISA account for his baby daughter, and uses the Invest account to invest small amounts into ETFs.

This is a review of the Trading 212 Invest account – the other account types available to you are Trading 212 ISA and Trading 212 CFD.

The CFD area is not covered in this review – we do not invest in CFDs due to the huge risk involved – we see it akin to gambling. After all, almost 80% of retail investor’s lose money with CFDs

Briefly, one use of CFD’s is to use leverage to make money on short selling, but beware – leveraged gains mean there’s a chance of leveraged, or magnified, losses.

You are also charged for overnight positions, so they’re no good for long term investing. We say stay away! Now, back to the review…

Yes! Well, nearly. There are certainly no trading or platform fees, but surely there must be some hidden fees? How else do they make their money?

This is the first question we ask when confronted with a free offer – what’s the other side getting out of it?

Well, Trading 212 are indeed offering a free service on their Invest platform, with the hope that you will use the CFD area of the site as well, and other future products such as robo investing, for which they intend to charge.

It’s a classic freemium model – the parts that most people will want to use (the stocks and ETF markets) are offered for free, with their profits coming from more niche developments.

Sort of how banking works in the UK. Most people get a free current account, paid for by those that use the banks debt facilities such as overdrafts. Basically, someone else overpaying so that YOU get a free service.

It’s worth noting that even the ISA is fee free – Freetrade, another free stock trading platform that we reviewed recently, plans to charge £3 per month to use their ISA, but Trading 212 does not charge for this – a win for Trading 212 against the competition.

So come on, what are the hidden costs. There are always hidden costs with investing and Trading 212 is no exception – though these are not the fault of the platform, and it seems Trading 212 really have done their best to be cost free.

1) Stamp Duty

You will pay stamp duty taxes on the purchase of UK shares, but nothing for funds. UK Stamp duty is 0.5%, which is an immediate hit to your portfolio when you buy a share. But in all fairness, this is a tax and not a fee for Trading 212.

The share price would have to move up by this amount just to break even. And that is before considering:

2) The Bid Offer Spread

Trading 212 is a stock trading floor like any other in that shares and ETFs have 2 prices: a buy price, and a sell price.

The difference is called the spread, and this is the amount of money you would lose if you bought a share and immediately sold it.

A typical spread on a share in Tesco is around 0.04% on the platform.

It’s the kind of cost you should be aware of if you trade frequently, but most long term investors will not notice such small amounts.

3) Foreign Exchange Spot Price

Not a concern on Trading 212 Invest – When buying foreign shares, of which there are 1,093 at time of filming, you would usually be charged a foreign exchange fee on most platforms – Trading 212 doesn’t and translates at the spot rate.

It’s worth noting that competitor platforms do charge a fee – for example, Freetrade adds a 0.45% charge on top of the spot rate; but Trading 212 does not.

Another reason why Trading 212 is currently the superior platform in terms of price in our opinion.

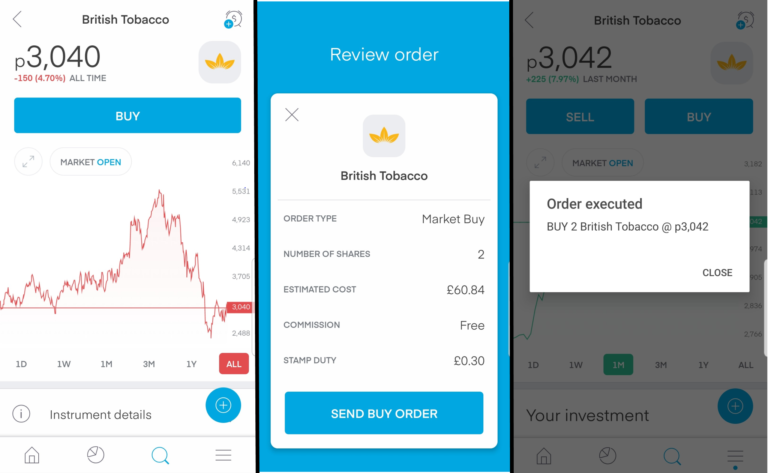

Ben used the app to buy shares in British Tobacco. Again, Trading 212 was superior to the Freetrade app as the trade was carried out instantly without paying extra. See how the price was 3,040 just before he clicked the Buy button.

The competitor platform Freetrade batches trades together and executes at 4pm, so prices can move during the day but Trading 212 traded at such a current price that it had moved to 3,042 in the fraction of a second it took to load the next screen. Note that the minimum number of shares you are allowed to buy in a stock is 2 shares. Also note that stamp duty is already hitting this portfolio by 30 pence.

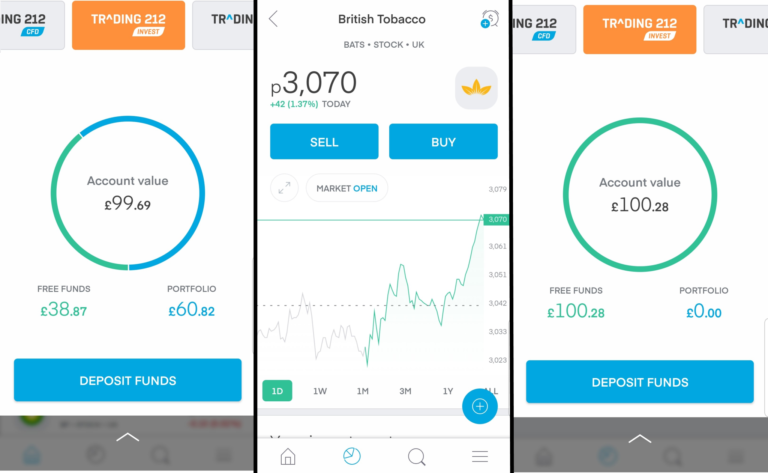

Ben locked in the price and executed the purchase at 3,042. What started as £100 went down to £99.69. Why? Two things happened in the intervening seconds. One was he’d been taxed stamp duty of 30 pence, and the other is the market had moved down by a penny. These price updates are lightning fast!

Later that week, he took advantage of a rise in the share price to sell the shares and test how well the app handles sales. He sold the 2 shares in British Tobacco at a price of 3,070, just by clicking sell, and confirming the sale.

Seconds later, the portfolio value was confirmed as £100.28 in Free Funds, a.k.a cash; therefore the sale had been instantaneous. He’d made a profit of 58 pence, after the 30p stamp duty, in a week.

Interesting sidenote: If we could replicate that return every week, that would £30 a year return on £100, or 30% rate of return. There’s definitely value to be found by having this app in your pocket, though we encourage long term investing over trading.

At time of filming there are over 1,500 stocks (of which 450 are UK stocks) and 223 ETFs on the app to choose from.

This is quite a decent range in our opinion for a free app.

It doesn’t offer nearly the wide range that a big platform like AJ Bell or Interactive Investor offers, but it offers enough for you to dabble in many interesting markets.

Want to invest in cannabis, healthcare, automotive, tech, finance, America, Europe? You’re covered.

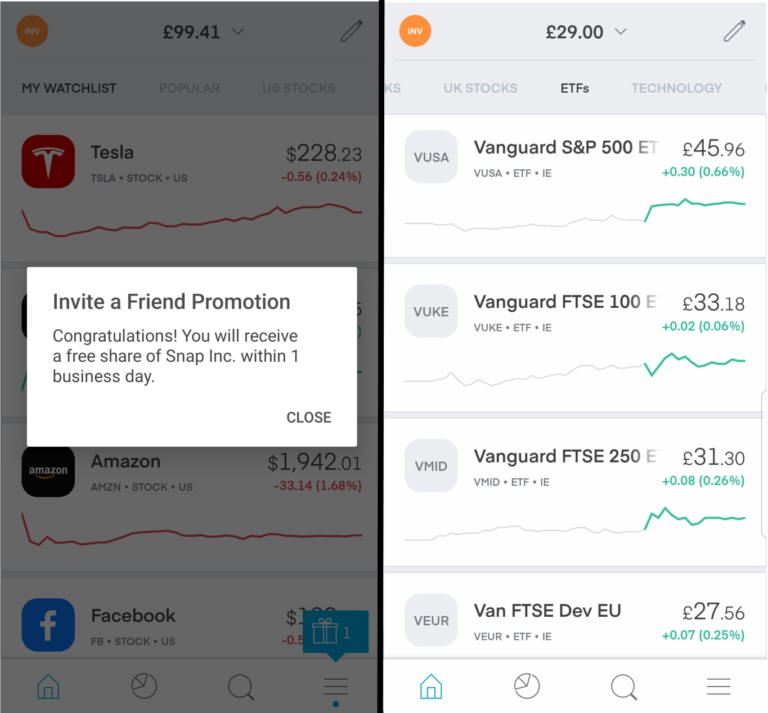

What we love more than anything else is that Trading 212 has some of the main ETFs from the Vanguard family, including the FTSE 100, FTSE 250 and S&P 500 ETFs. These funds are perfect for beginners and pros alike, and would be what we would be investing in first.

It’s bonus time! Sign up to Trading 212 Invest through our offers page here and you will be given a randomly selected free share by the app, which could be worth up to £100.

You just need to open an account, deposit £30 and you’ll get your free share within days.

(Probably best to deposit a little more than the minimum as the stock market can move down as well as up, and you don’t want to miss out on your bonus on a technicality!)

So – do you think Trading 212 is the future of stock market trading? Are you happy with the trade-off of less choice for lower fees? Let us know in the comments below.

Is it OK to invest in sin stocks? Sin stocks include companies who deal in gambling, alcohol, tobacco, firearms – basically anything immoral.

Any companies that make a profit are OK in a sin stock portfolio, regardless of whether they are a cigarette company selling addictive or harmful products, firearms dealer, or a financial giant encouraging the vulnerable into bankruptcy for their own profit.

But shouldn’t investing just be about the returns? Are we trying to set ourselves financially free at any cost? And how do sin stocks compare against the returns found in socially responsible funds?

YouTube Video > > >

The reason investors buy stocks and funds of companies that act immorally is because the returns are thought to be much higher, and more consistent, than other stocks.

Take tobacco for example. Despite public smoking bans in the UK, British Tobacco has cornered the market on an addictive product that consumers the world over see as essential – revenues are practically guaranteed, as are the dividends to investors.

Things like tobacco, alcohol and war are not going away anytime soon, and the profit margins there can be huge.

For investors just wanting to retire rich, the argument goes “why wouldn’t I buy the best stocks to achieve that target”, when the world’s problems aren’t going away by choosing not to buy those stocks.

One could argue that these products are only fulfilling someone’s desire, so perhaps are not even immoral in the first place.

At the other end of the spectrum are funds that specialise in Socially Responsible Investing.

SRI fans prefer an investment strategy that promotes responsible, liberal, green and cuddly corporate behaviour with a feel-good factor above investment returns.

Such funds could make phenomenal returns – but it would be a coincidence, as the main criteria for companies to be in these funds is meeting some fund manager’s definition of “socially responsible”. Token KPIs such as having more women than men on the board of directors could be a qualifier.

More women on the board of directors is a fantastic objective, and one that we fully support, but focusing on who is employed on a board is not the same thing as having a solid investment strategy for the shareholders.

While it is undoubtedly a good thing to promote equality, your retirement strategy should not be dependent on funds whose primary purpose isn’t making you money.

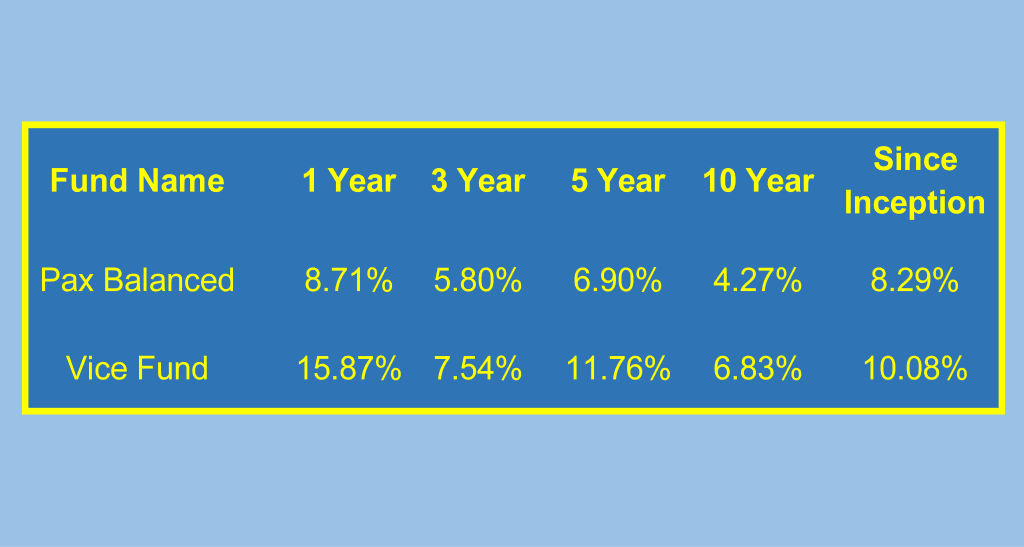

Let’s look at a couple of US funds as examples. The Pax Balanced fund, launched in 1971, is the oldest operating SRI fund in the business.

The Barrier (or Vice) Fund, launched in 2002, is the industry’s oldest sin fund. Let’s compare the two.

The first table shows that the sin fund has done better, smashing market averages, probably because it focuses on making money instead of identity politics:

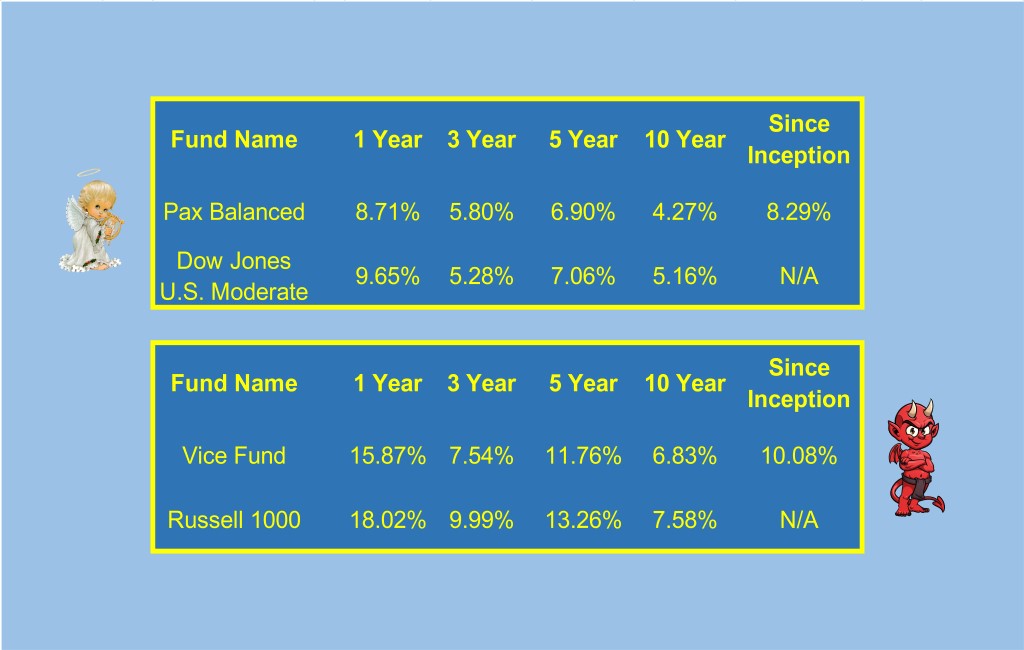

However, comparing the funds to their respective indexes tells a different story. The socially responsible fund performed a little under the market index, but the vice fund fell short by quite a way. Maybe it doesn’t pay to sin after all.

These numbers suggest to us that cuddly SRI funds can perform to around the market average, though we suspect that is due to diversification and good management – SRI companies do a tend to have well-formed management structures.

While, it might actually be better to invest in the Russell 1000 and track this index, rather than invest in the sin funds that single out specific companies.

But history can’t tell us the future, and the sin stocks were still performing well above the 7% or so that is usual for markets more generally.

Based on the history, there isn’t a conclusive win for either camp – and it was a limited comparison anyway between 2 funds, so isn’t definitive.

It comes down in part to your own moral code. We would suggest avoiding both extremes, and settle in the middle with top rated companies who make good money for their investors and will allow you to retire comfortably.

One thing to note is that many of the so called Socially Responsible funds invest heavily in big technology, pharmaceutical and financial services – probably why they are able to get returns that are almost as good as the market!

Also, as SRI is the in-thing at the moment this might be elevating valuations – People are prepared to pay more for an ethical stock. Likewise, this could be suppressing sin stocks.

Many SRI funds have also dropped their exclusion of alcohol and gambling – we can’t see the logic as to why these are not unethical but other things are, though it at least gives them a chance to make some decent money for their investors!

Likely a result of the breakout of snowflakery across the western world, SRI funds vastly outnumber sin funds.

There are dozens of SRI funds, including a number of exchange-traded funds (ETFs).

On the sin stock side, there are only enough to count on one hand, even with ETFs included, although there are plenty of individual stocks to choose from.

So you can easily (if not necessarily cheaply) construct your own portfolio of sin stocks.

If you’re just looking to make a solid investment, political views aside, a diversified portfolio that focuses on its shareholders will serve your financial interests better.

We don’t specifically target Sin Stocks, but we both happily invest in something like British American Tobacco.

We would not invest in any companies who were overtly immoral in their practises and these companies would not likely survive anyway.

Likewise, we would not invest in companies who prefer to make a political point with their shareholders’ investments, rather than profits – it’s all about balance.

Would you invest in sin stocks? Let us know in the comments below.

If you’re not careful your investment pot can be decimated by platform fees and trading fees amongst other charges. But with the launch of the Freetrade platform, we’ve got some exciting news for UK and even European investors – a shift that will hopefully change the investment world forever.

One of the biggest barriers to investing for young people or even people of all ages for that matter, is the cost of investing. Well, all that is beginning to change with the introduction of zero-fee, that’s right, zero-fee investment platforms such as Freetrade, Trading 212 and there’s even more on the way.

You can now invest for completely free!

YouTube Video > > >

The US has been the leader in this market disruption when Robinhood entered the scene in 2013 but us UK investors were still left paying sky-high platform and trading fees until relatively recently.

Is Freetrade the revolutionary investment app that we’ve all been waiting for?

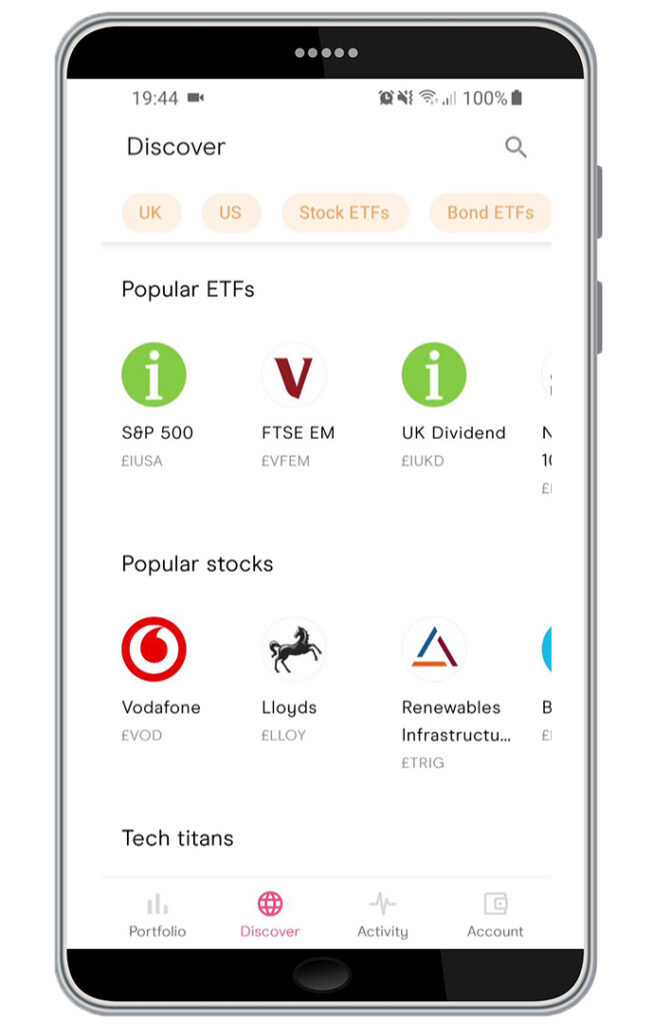

According to Freetrade themselves, they are a challenger stockbroker providing free stock trading. There are no fees on basic trading, and they are able to do this by driving down their own costs and charging small amounts for “premium services.”

Freetrade is available on both Android and iPhone and with Andy having personally tried and tested the app with a small amount of his own money, we can vouch that it is very easy to use.

Looking at the key points:

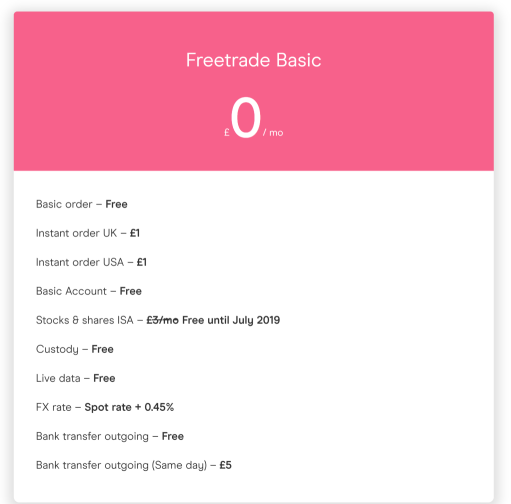

Free isn’t it? Well, not exactly. It could be completely free for some but for most investors it will come with a very small fee.

Normally when you buy shares you get a live price and you execute the trade there and then. But Freetrade are collating all the trades and executing them all together at 4pm daily to cut their admin costs. This does mean that you won’t actually know the price before you buy which could be dangerous. On a normal day the price won’t change much but on occasion prices can skyrocket.

Imagine if there had been a takeover announcement and the share price had rocketed up 30%. You now would be paying way more than you had expected.

We actually really like this feature as it’s a way to cut trading fees, but we would like the option to set a maximum price just in case the situation changes. Let’s hope Freetrade are listening to this video.

Alternatively you can place an Instant order where you can execute the trade immediately, but they will charge £1 for this service. Our rule of thumb is to try and keep our trading costs below 1%, so we would make sure we at least invested £100 per trade but there is no actual minimum set by Freetrade.

The use of an ISA will cost £3 per month but you may not even need an ISA. We personally would always try and use an ISA as we plan on having huge sums of wealth.

But because UK residents get a generous capital gains allowance and a £2,000 dividend tax allowance, then many investors won’t ever pay tax anyway, so don’t need an ISA. Think about your own circumstances and act accordingly.

And finally there is a reasonable – but note – not free FX fee of 0.45%. Don’t forget that you could be trading in US stocks priced in dollars and even many UK companies pay dividends in dollars, so you will incur this small fee.

So far, we are very impressed with the price, but this is where things begin to unravel. We have previously been spoilt for choice by more traditional platforms where you can invest in practically everything you can think of.

The most notable absence is funds such as OEICs and Unit Trusts.

They do offer a small number of ETFs, but we would expect traditional funds to also be available. The good thing about Freetrade is their transparency and they do provide a spreadsheet listing what is available but sadly at the time of writing this only contains 358 stocks and ETFs. In fact, they offer only 43 ETFs.

Now, they are updating this all the time and you can request they add something but there’s no guarantee you’ll get what you want.

One of the biggest absentees in our opinion is the family of Vanguard LifeStrategy funds. We believe these are great for beginners. Considering Freetrade is aimed at new investors we feel these should at least be included.

It’s fast, streamlined and not cluttered but doesn’t really offer too much. It would be nice to see some Stock or ETF information such as dividend history, yield and stock allocation.

Even when clicking on the max price graph, it doesn’t even indicate what time period it is for. You do get a brief description of the stock or ETF, which is nice and of course the key investor document.

There was so little information it means that you must go online to research everything first and can only really make the trade on the app itself. But perhaps this is a price worth paying in order to get zero-fee trading.

One major flaw is the lack of a trading website. We like having the option to download or even just view my portfolio on a desktop, so we can carry out some serious analysis on our portfolios. This isn’t possible on the small screen.

Whenever we have spoken to them, they have been helpful and quick to respond but the only way to contact them is with online chat. If you have a lot of money invested, you may feel you want to speak to a real person but will be unable to. We suppose this a key way to keep the cost down.

You bet it is, but we won’t be moving our investments to the platform just yet as we want wider choice and additional service that we feel is worth paying for. Also, as your pot grows the cost of investing comes down as a percentage of your pot, so personally the general cost of investing isn’t too much of a problem for us.

But for those with little money or those that don’t want any bells and whistles, Freetrade might be perfect for you. In fact, it is now truly possible to invest with just a few quid.

We also see or at least hope that traditional platforms will have to adapt, to prevent a huge exodus to these challenger brokers. As a result of these apps, we expect prices to come down across the industry in time.

What do you think of Freetrade and will it change the investment game forever? Let us know in the comments section.

We’re proud to bring to your attention a brand-new investment app which could be ideal for beginner investors in the UK. We know that one of the biggest barriers to investing is the perceived complexity, and perhaps the opinion from most people that it’s just not cool.

The Wombat Invest App plans to change all that by “empowering generations to manage, save and grow their money” in their words.

This app has some cool features that we think that many young people and beginners are going to love!

Editors note: Don’t forget to check the Offers Page and grab free shares worth up to £200, plus £50/£75 cash backs when you open new investment accounts through the affiliate links there!

YouTube Video > > >

In order to bring you this hot-off-the-press information and be amongst the first to review this app, Wombat gave us a small amount of credit to thoroughly test the app, on the condition that we had the freedom to provide an unbiased review.

We have remained impartial we will be covering the things we love and things we don’t love.

Wombat is a brand-new investment app available on Android and Apple devices that is making investing accessible to the masses. One of most commonly discussed problems with investing is the cost but it can also be very complex.

Even if you spend enough time learning the basics of investing it can still be needlessly complicated.

For instance, let’s take this ETF as example:

Ishares Dow Jones Global Sustainability Screened UCITS ETF

Most people will have no idea what that means, making it very difficult for beginners to even start.

It might as well be written in a foreign language.

Wombat will simplify all this for you as they have packaged investments into themes. Each theme invests in an ETF and we think the snappy names and description are far easier to understand for the average person than the complicated investment product names found elsewhere.

That ETF we just looked at by the way is actually the underlying fund that ‘The Goodies’ Theme invests in. We think you’ll agree that ‘The Goodies’ is far easier way to say that that the fund invests in socially responsible businesses.

A great thing about Wombat is it makes it simple for the novice but gives you enough detail for those that desire to know more. On the app you can easily view the fund fact sheet, KIID and prospectus.

It’s worth noting that Wombat does not currently offer investments in individual stocks.

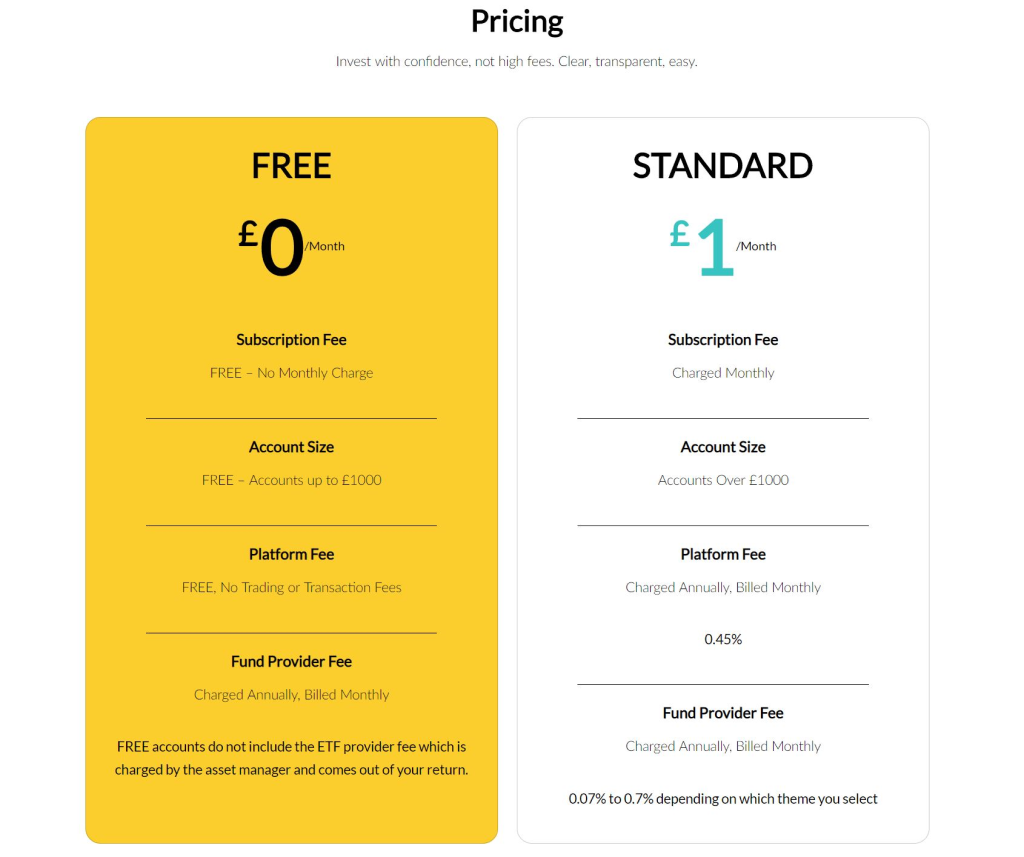

For those with small pots, fees can often decimate returns and we think that Wombat have been fairly competitive.

Usually the worst time for fees with many platforms is when you have a small pot. Wombat have amazingly [to find axe image maybe] taken an axe to all their fees when your investment pot is below £1,000.

We can’t stress enough what great news this is for those just starting out!

For those with pot sizes over £1,000 the prices are roughly in line with other platforms; but you need to be careful.

They’ve gone for a fixed monthly fee of £1 and a platform fee of 0.45%.

The 0.45% is perhaps a little high and they may struggle to attract investors with large pot sizes.

Having said this, this fee includes the use of an ISA, which you often must pay extra for on other apps, such as what Freetrade intend to do.

Unlike other platforms however you don’t need to pay extra for additional features.

As for the £1 monthly fee, this is practically nothing for those with a larger pot but if you have a small pot it can be on the rather steep side as a percentage of your pot – but of course it’s waived below £1000.

You’ll want to grow your pot quickly to minimise the impact of this fixed fee.

In fairness though, if people start investing because of this app we feel that it’s a price worth paying. You will almost certainly be better off financially by investing than never investing at all.

Here at Money Unshackled we have longed encouraged the behaviour of paying yourself first, which means you either save or invest money as soon as you get paid.

Although this is best practice most people don’t or won’t always do this. So, a nice little feature Wombat offer is called ‘Round Ups’.

What this does is round up your purchases and every 2 weeks it will pay the accumulated ‘Round Ups’ into your Wombat Account.

Hopefully you’ll build up a nice little investment pot without really noticing.

Obviously for this feature to work they will need access to your banking details, so they can securely access your transaction history, so they can calculate the required ‘Round ups’.

We expect this is no problem for the tech-savvy youth of today.

The app is slick and easy to use. You can buy into a fund with just a few taps and set up auto invest. They have some nice charts, enabling you to track your portfolio size and see projections way into the future.

The app even has a Learning Hub where you can find interesting and very helpful articles that should hopefully improve your investing knowledge, so we encourage you to check that out.

Sometimes you want to buy into an investment, but the ETF price is way too high, which may mean you can’t buy it at all, or you can’t get your desired allocation percentage.

This isn’t a problem with Wombat as they offer a very cool feature known as Fractional Investing.

Instead of having to wait until you have enough money for 1 fund you can invest in a fraction, meaning you can invest no matter how little money you have.

This again is unusual for an investing platform, and welcome. Some funds can be priced at hundreds of pounds just for 1 share.

On another platform this might be too much for you and may prevent you from diversifying properly – not the case on Wombat thanks to fractional investing.

As we’ve been in touch with Wombat, we’re very pleased to share with you some of the great features on the horizon, which we think will really enhance the app.

This includes individual stocks, so people will be further able to customise and tailor their experience. We always think new investors need to tread carefully around stocks, but there’s no doubt that they’re in demand by most new investors.

They’re also working on a “Wombat Junior” App, which will allow those under 18 to invest and “Wombat Gift”, which will allow people to offer investments as a gift.

They mentioned a lot more, which we’re not at liberty to say just yet for confidentiality reasons but it must be really exciting times at Wombat HQ.

To summarise, you can find cheaper ways to invest but we feel that its prices are competitive enough and combined with its great app and simple themes-based approach the Wombat Invest App will prove very popular.

Of particular interest to us were the Round-Up feature and the Fractional Investing feature.

We’re disappointed that we can’t buy individual stocks, but we’re told will be possible soon. If you want to invest in diversified funds this is a top-notch app. When the word gets out, we can see this being very popular amongst new investors.

What do you think of the Wombat App and will you be checking it out? Let us know in the comments section.

Updated: 27th November 2020

How would you invest £1000? We get asked this a lot. Should you invest in stocks and shares, equity funds, gold, property, exchange traded funds, peer to peer lending? And how much should you hold in cash?

In this article we’re looking at some of the best options for investing £1000; including what we would do.

For a more recent discussion on how we’d invest £10,000, check out this video next:

There are a lot of investment options available to you with £1,000, but if you only have £1,000, you should make sure that your money is accessible, in case of emergency.

The only truly liquid asset is cash – we’re saying that you should have an emergency fund of cash saved in a bank to fight financial fires with, and if you only have £1,000 in the world, a cash account would be the place to start.

Unfortunately, one of the main rules of investing is that liquidity is best when return is worst. But some banks offer Regular Saving accounts with decent interest rates, even in this post-crash era.

£1000 is more than enough money to invest in stocks and shares, funds and ETFs.

Many platforms including AJ Bell allow you to invest from as little as £25.This is one of our favourite all-purpose platforms, with amongst the best fees for small pot sizes.

So you can buy shares with £1000, but should you? Unless you just want to practise investing and don’t mind losing your money, avoid buying shares at such low amounts.

We’ve said elsewhere that we think the minimum pot size needed to buy shares is more like £6,000 than £1,000 – unless you’re using a commission-free platform.

The problem with buying only £1000 of shares is that you are unlikely to be diversified enough, unless your platform offers fractional shares.

Due to crippling trading fees on the standard trading platforms, we would spend a minimum of £1000 on each stock to get decent value; so it’s almost like you are gambling rather than investing, as you would only hold one card in your hand. Maybe it does well – maybe it doesn’t.

However; there are now some new “free” platforms get around the problem of fees, making buying small amounts of shares more realistic platforms such as Trading 212 and Freetrade, but are limited in the number of companies and funds on offer. Shares and Funds alike can now be bought fee free! – amazing.

CASHBACK OFFER for our readers: if you want a free share worth up to £200, simply sign up to Freetrade through the link on the Offers page.

ETFs are amazing because they track stock market indices without needing expensive fund managers, have very limited fees and can have very high diversification.

One great place to buy ETFs is on the Vanguard Platform. Their FTSE 100 and S&P 500 ETFs are ridiculously cheap in terms of fees, and track the market almost perfectly. Some of our all-time favourite investment products.

Managed investment funds are certainly a respectable place to invest your thousand pounds. They are often well diversified across many companies, sectors and geographies.

The problem we have with managed funds are the management fees. Fees on actively managed funds can be quite damaging to long term returns. Sometimes that fee might be worth paying.

And even then, not all funds are expensive. Vanguard also offer funds, including funds of funds!

Vanguard LifeStrategy Funds are collections of other funds and ETFs in one package – a one stop shop for access to a significant chunk of the world markets in one ultra-diversified investment.

The fees are ridiculously low too which we love. If we were starting out in the stock market, we would either start here, or with S&P 500 and FTSE 100 ETFs.

So how can we invest and diversify in the stock market with limited knowledge?

Do you want to invest your wealth without having to think too hard, for minimal fees, and with some investment advice thrown in? Then try a robo investing platform.

We would use an established platform like Nutmeg. With even small amounts of money, you get access to basic investment advice, which otherwise would have been unaffordable, and Nutmeg will make the investment decisions for you based on how you answer their questions.

You can even get 6 months without fees if you use the referral link on the Offers page – remember, fees should be avoided at all costs!

Peer to Peer Lending is a good mix of decent returns, lower risk, and increased liquidity compared to the stock market. Since the coronavirus pandemic strated however, P2P platforms have mostly put themselves on freeze to new investors.

Some are still accepting new customers though, including Loanpad and easyMoney – again, cashback offers are available for these on the Offers page.

Only buying commodities with £1000 wouldn’t give you much diversification.

You could buy some physical gold bullion or invest through an ETF, but gold doesn’t pay a dividend. It is a defensive asset though that could be useful in a downturn, but not essential when you’re first starting out small amounts of money.

For £1000? No chance. You can invest in funds that invest in commercial and residential property, but to buy an actual buy-to-let rental property with the leveraged returns that come with it requires a cash outlay of £30k upwards. Keep this one on the back burner for when your pot is bigger!

Where will you be investing next? Let us know in the comments below.

Investing for beginners can seem very daunting but it doesn’t need to be this way. In fact, investing is incredibly easy if you spend a bit of time learning the ropes. Just a few minutes here and there could shave decades off your working life and set you financially free.

YouTube Video > > >

We regularly get asked this as if we have got a secret investment opportunity that somehow gives safe and yet enormous investment returns with instant liquidity. Liquidity refers to how easily assets can be converted into cash at its intrinsic value.

This means the value determined through fundamental analysis without reference to its market value. Or more simply what it should be worth even if the actual price is different.

So, property is very illiquid, as it can take several months to sell, and you may have to sell below its “real” value. And with stocks and shares you might be able to sell quickly but you may be forced to sell below its intrinsic value.

An emergency fund must be accessible and not prone to sudden value declines. This means the only place to store an emergency fund is in cash, whether that be in physical cash or a bank.

All is not lost as you can take advantage of some savings accounts and even higher interest regular savers on the proviso that you have instant penalty free access.

Unfortunately, an emergency fund is just one of those things we must all have despite inflation destroying its value.

In time your other assets will dwarf it, so the fact your emergency fund is doing nothing won’t be such a big problem.

You can generally start as low as £25. But often it’s not the forced minimum you need to be concerned about- It’s the minimum required to have a diversified portfolio that you need to be aware of.

If investing just in stocks, we traditionally would have said £6k in order to get basic diversification but with new “free” platforms, you can practically start with nothing.Of course, we never encourage beginners to start with a purely stocks-based portfolio due to the risks.

If you go down the fund route, which we always encourage, most traditional investment platforms have a minimum monthly investment of £25 and a monthly trade cost of about £1. But it’s better to do more than £25 if you can to reduce the impact of the regular trading fee.

You might be thinking“I’ll go with the free platforms”; but be aware they are limited in the service they offer and the investment choice.

This must be the most frequent question along with “what platform do we use?” The truth is there is no single best platform and what we use is probably not right for you, as there are so many different variables. It also depends on what account you are using such as ISA, SIPP and so on.

Perhaps we can summarise the platforms into categories and you can choose the one best suited to you:

Some people mention trading sites such as Plus500 or etoro but these are not investment platforms.These are trading platforms where you trade CFDs. We don’t currently gamble in CFDs and something like 80% of those who do, lose money.

Long term we will probably flourish and that is whether we are in the EU or Out. We’ve never understood all the negativity. The best approach is to just decide and get on with it. Indecisiveness is the only problem.

Personally, we both think we will be better off out long term but Britain is a great country and has been for thousands of years- This will continue either way.Leaving without a deal would probably see short term issues as we need to arrange so many things that we as a nation haven’t been responsible for, for decades.

And of course, some companies would want to adjust their operations. Perhaps to get better access to Europe and perhaps better access to the UK.Whatever you do, make sure you have a global diversified portfolio and laugh at everyone else worrying over nothing.

We have regularly promoted the Vanguard LifeStrategy fund as a great fund for beginners because it is dirt cheap, and has enormous world diversification but with a UK focus.

But we often get asked whether they should buy this fund or that fund to go with it. This could be the Vanguard S&P500 as an example.One of the main reasons to buy the LifeStrategy fund is because it’s a one stop shop. You don’t need anything else.

In our opinion the only reason to buy another fund is if you wanted to adjust the allocation. For instance, if you thought the LifeStrategy fund was too UK focused you could indeed buy some more S&P500 to alter this.

Just be careful that you are not altering it with the intention of increasing diversification, as in reality, you could be lowering it.

What other money or investing questions need answering? Let us know in the comments section!

The impact of platform fees, trading fees and management fees on an investment portfolio can be disastrous to long term success – add in taxes, and the impact can be catastrophic.

Below we’ll work through several examples of how a person might invest their money in the stock market – what we think the best method is – and show how fees and taxes can wipe almost half off of your portfolio’s value.

YouTube Video > > >

In these worked examples we assume that an investor is regularly saving £250 a month into an investment platform, achieving a return on investment of 6% after inflation. All long term forecasts have inflation factored in, so show the real money returns.

Unless you are an expert, you might expect to get similar returns from investing in shares as you could investing in Funds or ETFs, at least this is the assumption we have used.

If you are investing in the stock market, you are going to have to navigate a whole ecosystem of fees.

Fees for making trades, fees for using a platform, fees to pay a Fund Manager’s salary, and a whole bunch of hidden admin fees that investment platforms and funds are less-than-transparent about revealing.

At Money Unshackled, we have long promoted low fee stock market vehicles such as ETFs, exchange traded funds, over more Fee-heavy vehicles of Managed Funds and even buying individual stocks directly, and now we’re going to show you why.

In green is our baseline – it’s how big our investor’s pot would be if left to grow over a 30 year term, adding £250 a month and compounding at 6% net return from growth and reinvested dividends. £244,000! Not a bad little pot to retire on.

30 years of industrious saving and investing giving you a result you deserve. But let’s now consider Fees.

ETFs generally have the lowest fees. We’ve used as our example the Vanguard FTSE 100 ETF on the Vanguard platform, which has total fees of 0.26% – cheap as chips! Incidentally, their FTSE 250 ETF does have high transaction costs built in, making the total fee 0.4%.

For our example, we’ll use 0.26% as our example total ETF fee… and ask you to think twice about hidden transaction fees when you choose your ETFs!

If we’d invested in ETFs (the blue line in the chart above), our after-fees total pot size barely moves – we’re able to walk away with £233,000 with fees barely making a dent on our retirement.

Managed Funds on the other hand are notorious for having high hidden fees. A popular UK fund we use an example is the Investec UK Alpha Fund J GBP Acc:

Total Fees on an example Fund: around 1.2% plus £12 a year

Investing in this fund will cost you 1.2% total fees. 1.2% doesn’t sound much, but consider that 1.2% knocked off your assumed 6% return gives you only a 4.8% return after fees. As we’ll see, the effect of this can be huge.

If we’d invested in Managed Funds (the orange line in the chart above), we’ve paid Fund Manager’s salaries and other costs of tens of thousands of pounds over the years, leaving us with only £196,000 to spend on ourselves.

And finally, by buying shares individually you will incur lots of different fees, including but not limited to ongoing platform fees, stamp duty on trades, and regular platform trading fees.

You will need to regularly rebalance a portfolio of shares to keep your portfolio performing – we estimate this costs £200 a year on a 20 stock portfolio: 20 trades a year at around £10 a pop.

Other fees are stamp duty on rebalancing: which might be 0.125% a year on our portfolio [0.5% stamp * ¼ of our portfolio each year] if we assume we annually rebase a quarter of the value of our portfolio, platform account fees of, let’s say, 0.25%, and another £45 a year for trading and stamp duty on new deposits.

Total fees an example individual stocks portfolio = 0.375% plus £245 a year.

If the investor thought that they knew best and invested directly into shares, returning the same as a Fund manager could achieve, they’d have performed a little better after fees, keeping £210k to play with in retirement – the purple line in the chart above.

Of course, this assumes you know what you’re doing and are able to get the return before fees as a Fund Manager! And that you don’t have an itchy trigger finger and trade even more frequently!

The effect of fees is truly scary – the moral is, unless you think you can beat the market, tracking the market with an ETF will generally pay off better. It’s all in the Fees.

Don’t forget that as an investor, the government feels it is entitled to take chunks of your invested savings for itself, despite you doing the “right thing” and planning for your future.

By investing, you will be less of a burden on the state as you will be able to sustain yourself through retirement rather than rely on the government for handouts, but this point is lost on the Treasury.

In any case, if you invest without shielding yourself from tax, you will be stung, and stung hard.

Tax is largely dependent on your circumstance, so let’s show a high level assumption of what out investor’s pot would look like as a higher rate taxpayer if he invested in ETFs vs Managed Funds, after fees.

A higher rate taxpayer will be taxed a crippling 32.5% dividend tax! We’ve assumed half of your return comes from dividends, and have factored in the £2k dividend tax threshold.

Starting again at our baseline (the green line), lets now look at what a higher rate taxpayer would expect to keep investing in ETFs and Funds. A higher rate taxpayer might keep only £208k investing in ETFs (blue), while a higher rate taxpayer investing in Managed Funds (orange) might only keep £176,000 of their potential pot size – on the way to half your pot being lost to Fees and Taxes!

There is of course a way to protect yourself from Taxes. Just like ETFs have been created to avoid Fees, ISAs have been invented to avoid taxes – and legally.

A Stocks and Shares ISA works much like a regular Cash ISA, in that the returns within are shielded from taxes.

There are some exceptions that can’t be avoided, such as US Foreign Withholding Taxes of 0.15%, but for a UK investor investing solely in UK stocks this shouldn’t be an issue for you.

The ultimate Fee and Tax busting combo is therefore an ETF based portfolio, built up through an ISA, as below:

Of course there is still reason to buy stocks and shares directly alongside ETFs, and we do this ourselves – if you know what you are doing, and have seen an opportunity for market beating value, it is of course possible to do better than the scenarios detailed here.

But for most of us, following a strategy of Fee and Tax minimisation is the key to a successful long term investment plan.

Have you put much thought into Fees? And are you making use of your ISA allowances? Let us know in the comments below.

We get asked this question all the time – What is the best investment platform? But sadly, there isn’t a clear-cut winner. It all depends on the service or functionality that you want and the amount of money that you have invested and your investment style.

Previously we’ve praised Interactive Investor for those that have a decent amount invested. But from the 1st June 2019 they’ve introduced new charges. So, does Interactive Investor still cut the mustard?

Here we review Interactive Investor and see if it’s still the best investment platform for UK investors. Let’s check it out…

YouTube Video > > >

Interactive Investor offer a wide range of accounts including ISA, SIPP, Junior ISA and General Trading Accounts. We expect these as standard but it’s not uncommon for other platforms to only offer a general account, which means you could be liable to pay taxes on your gains and dividend tax.

So called “free” platforms such as Freetrade do offer an ISA but have additional charges for these. So, Interactive Investor including all these accounts as standard is great but note there wasn’t a Lifetime ISA option, which might be a disappointment for some of you.

Of course, those that watch our YouTube channel on a regular basis will know we strive for financial freedom today, so the standard Investment ISA is our weapon of choice.

Generally, there are 2 type of fee structures for investment platforms: –

As you can imagine you don’t want to be paying a percentage fee if you have a lot of money.

For example, AJ Bell offer a low percentage fee of just 0.25% but if you’ve managed to build up a large investment pot of say £200,000, that 0.25% would be an annual charge of £500.

If you have built up a pot £500,000, which you might do if you’re serious about financial freedom then it would be a charge £1,250.

This is simply getting ridiculous on the larger pot sizes.

This is where the white knight Interactive Investor comes riding in to save us with their friendly flat fee pricing. No matter how much your pot size grows Interactive Investor are going to charge you the same amount.

They used to offer what we thought was a very good price at £90 per year (£22.50 per quarter). But sadly, they just increased this to £10 per month, so £120 per year.

Despite the disappointment with the cost increase it doesn’t really change too much, albeit you need a little more money to make Interactive Investor the lowest cost platform.

In fact, Interactive investor don’t just charge £10 a month. They’ve introduced 3 service plans at different prices with the £10 plan being the cheapest. Whilst this does make things more complicated to compare, it does benefit those that trade frequently, as you will get lower trading costs on the more expensive plans.

Here at Money Unshackled we encourage you to trade less frequently and hold for the long term, so we don’t really see the need to be on the more expensive service plans. Those that trade frequently tend to underperform due to clocking up lots of trading fees. Because of this we’ll be basing the rest of the review on the cheapest ‘Investor Plan’.

A positive change they’ve made is the reduction of trading fees from £10 to £8, which is a very welcome change indeed.

The great thing about Interactive Investor is they actually give you the equivalent of 1 free trade per month. This is £8 credit to spend on whatever trades you like, so really can make Interactive Investor a cheap platform even for those without a huge amount of money.

Unfortunately, those credits expire after 90 days, which isn’t long. We think under the old prices, they used to last 12 months.

Interactive Investor isn’t just a 1 trick pony. They have 1 of the best service offerings out there. And in their words, you “Get access to more investment opportunities than any other provider in the market”

This includes access to 40,000 shares across 17 global exchanges, over 3,000 funds, investment trusts, ETF’s and more. This superb range just isn’t provided by cheaper alternatives.

One of the features we like is Regular Investing, which allows you to invest on a monthly basis for just £0.99 per trade. We both feel that regular investing is one of the best ways to build significant wealth.

They also provide a dividend reinvestment service for just £0.99. Another service that many cheaper platforms don’t offer.

They also have a contact phone number…Wow! Don’t underestimate this. When you have a lot of money invested and you need help you may want to speak to a person. Not all investment platforms make it so easy.

To summarise, we feel Interactive investor is ideal for those with larger pot sizes, or even those that will have a large pot size in the near future.

The monthly free credit is also great, which depending on your frequency of trading can make Interactive Investor one of the cheapest platforms even for smaller pots.

What do you look for in an investment platform? Let us know in the comments section.

Unilever is one of the biggest companies in the world and yet many people have no idea who they are or what they do. But we guarantee that almost everyone has purchased their products.

Does their global reach and huge product range make Unilever stock an essential part of every investor’s portfolio? Offering an amazing dividend that keeps getting bigger and a strong balance sheet, surely this is the stock of dreams?

So, who are Unilever? How do their fundamentals look? What does Unilever’s future look like? And is it worth investing in?

YouTube Video > > >

Unilever are one of the companies we featured in our very popular Youtube video ‘Best Dividend Stocks UK’.

The company is a colossus with a market cap of whopping £127b, which is up from £109b in that previous video, so that’s some nice growth in such a short time.

Next time you’re in a supermarket or even just look in your cupboards and check out the manufacturer of those products. We bet a large majority of these are owned by just a small number of companies – Unilever being one of them.

In fact, according to Unilever, “Seven out of every ten households around the world contain at least one Unilever product.” They also own over 400 brands with 13 of these having sales of over one billion euros.

We love this company because brands, and lots of them, create a protective moat, which make it very difficult for competitors to enter the market. A protective moat is a key thing legendary investor Warren Buffet looks for when investing. Consumers tend to have loyalty with their favourite brands and keep coming back.

Not only does this give Unilever a more predictable income stream but it allows them to charge more than competitors – often a lot more. Take Domestos, Supermarkets tend to charge about £1 for a bottle but the non-branded supermarket version is around 45p – For essentially the same product. This is a whole lot of extra margin for Unilever.

They are also hugely diversified in terms of geographical reach with exposure to markets all around the world with particular exposure to emerging economies. It is these countries where large growth is expected to come from.

In fact, almost half their revenue comes from this area. Strong brands across many geographical markets make it less risky for investors…perhaps.

Remember as an investor you’re looking to stack the odds in your favour.

The dividend yield is certainly not the highest in the FTSE 100 but it’s still decent at 2.80% with a healthy dividend cover of 1.52.

A rising dividend with healthy cover is exactly what you want to look for when constructing a dividend portfolio. Unilever even pay out the dividend on a consistent quarterly basis, which is great for your cashflow.

Bear in mind that Unilever now decides dividends in euros, so while the dividend is consistently rising in euro terms, UK investors will see a level of volatility due to currency exchange rates.

Just look at that share price growth on top of any dividend payouts. Whilst a chart like this is historical and not necessarily an indicator of the future, it goes to show that performance has been good.

Whilst your investment style will dictate whether this is good or bad, we tend to like this consistent growth. Stocks that show sharp drops may look like opportunities, but it is far too common to get stung again as further drops often occur. I should know as I’ve been stung a few times myself.

We find the best place to go for information on earnings for any stock is the companies accounts. Investment Websites are good but can sometimes have errors. Unfortunately, annual accounts are long, complicated and extremely boring.

Revenue has hovered around the €50b mark for past 3 years but despite this they have managed to grow Net Profit and EPS. Bear in mind that we see a huge surge in non-underlying items. By following the notes, you can find that this relates to the disposal of its Spreads business. These sorts of gains are one-offs and should be treated as such when analysing stocks.

Whilst a full analysis of earnings goes beyond the scope of this article, we are happy with the company’s earnings.

According the Hargreaves Lansdown the P/E ratio is 19.80, which is based on the adjusted EPS – This is excluding non-recurring items, which we assume to be things like the disposal of the spreads business just mentioned.

This is high when compared to the FTSE 100 PE of about 15 but we think that Unilever has better growth prospects and certainly more protection against a price drop.

Unilever relies on the power of its brands. They need to ensure that their brands stay relevant.

Changing consumer demands and even new taxes such as sugar tax can have a huge detrimental impact on Unilever’s business. Then there is the problem with plastic packaging. Unilever needs to find a way to reduce its use of plastic.

Customers are becoming more concerned with the environment and are beginning to avoid products that unnecessarily damage the environment. There is also taxes and fines that will damage profitability if they don’t act on this now.

Do you like the look of Unilever Shares and will you be investing? Let us know your opinion in the comments section.

The Financial Independence, Retire Early Movement, or FIRE movement for short is a lifestyle choice to retire early by gaining financial independence at a relatively young age – usually aiming to retire in their thirties or forties at the latest.

In one way it’s something we’ve been teaching on our channel from the very beginning but never referred to it by its name.

YouTube Video > > >

When we talk to people about early retirement, we generally get 1 of 3 responses:

So, what is the FIRE lifestyle? How is it done? Do we agree with it? And can it really be achieved?

Although we think the concept of Financial Independence, Retire Early must have been around since the beginning of time, many of the main ideas have been credited to the best-selling book Your Money or Your Life, linked here, so make sure to get yourself a copy. If you learn anything from this book, then it’s been worth the price.

FIRE‘s formula is very simple: spend less than you earn and invest the surplus. FIRE is achieved through aggressive saving – and we’re not just talking about a bog standard 10-15%.

The objective is to accumulate assets until the resulting passive income provides enough money to cover living expenses in perpetuity.

If you can only save 10%, then it will take 9 years to save for 1 year of living expenses.

However, if you can pump those up to a 50% saving rate, then that is just 1 year of work to save for 1 year of living expenses.

Some people are able to go even further to 75% and beyond. Also factor in some investment growth and you’ll be financially independent in no time.

We can sense some people will think that’s impossible and that we, and all those that preach this stuff, are chatting complete bull.

Those seeking to attain FIRE intentionally maximize their savings rate by finding ways to increase income or decrease expenses.

The extent of how much you decrease expenses is up to you. If you can live off and are happy to live off rice, live in a tent and do nothing else, then you can probably save quite a high percentage of your income.

But most people, including us are unwilling to go to such extremes.

You can of course cut out all the unnecessary spending, and if you follow the teachings in Your Money or Your Life you will identify every single penny that comes into and out of your life.

This way you’ll finally see where you spend and potentially waste money.

We prefer to increase earnings, whilst being semi frugal.

Some ways we each maximise our savings rates is by increasing our earnings through multiple streams of passive income.

This includes ad revenue, which you may have seen on our YouTube videos and affiliate marketing.

We are also now live with the MoneyUnshackled.com website, which will bring more helpful information to you and hopefully an even wider audience.

Supporters of FIRE suggest the use of 4% as a safe withdrawal rate, meaning you would need an investment pot of 25 times your annual living expenses.

Of course, the 4% rule may be too high, but it could also be argued that you need far less if your investments perform far better than the stock market average.

A few investment properties could return 20%+. We’ve done a video on how this is possible, here.

Absolutely. Personally, neither of us would want to scrimp and save to the point life was no fun but FIRE is not much different to what wealthy people have done for generations – living off their wealth.

Achieving it is not easy otherwise everyone would do it. But if you can build your income and keep lifestyle inflation to a minimum you can definitely achieve it.

We’re both already on the path to Financial Freedom and would love for you to join us.

Upon reaching financial independence, paid work becomes optional – you don’t have to retire.

For some reason, many people get confused with what freedom is.

You are free to do what you want. If that is work, in whatever form, then so be it.

Are you or will you be living a FIRE lifestyle? If so, we want to hear how you are doing this. Let us know in the comments section.