Among the countless stereotypes about young people is the belief that they manage money poorly. How to manage money well is not something that is ever taught in school or University, but if you take the time to master the money game you will have it in abundance.

In this post, we’re discussing the 6 things you should know about money before you turn 30. The more of it you can earn and invest from as young an age as possible the better. You need to make sure you’re on top of all the points in before it’s too late. Now, let’s check it out…

FYI: Stake are giving away a free US stock to new UK investors, worth up to $150, to everyone who signs up via this offer link. More info on the Offers Page.

Alternatively Watch The YouTube Video > > >

Multiple Streams Of Income Is (Usually) Much Better Than One

Most people’s job income is their lifeline. If this is you and your wage income suddenly stops, you could be in serious trouble because you have bills to pay and responsibilities. In the event of losing that single source of income, the likely best case is you are forced to spend your savings, which means either your retirement will get pushed back or you’ll have to forgo whatever you were saving for.

But for many the outcome is far worse, with the loss of your home a real possibility and/or racking up a load of expensive debt. Most people have one job and depend on it like a new-born baby depends on its mum. They are totally reliant.

It’s common to think that a salary is a reliable source of income but ask anyone who’s been fired or made redundant, and they will tell you the exact opposite.

This powerful chart shows how many people were made redundant in the UK by month since 1995. The typical monthly figure is between 100,000 to 200,000 people. And during the bad times it has been 300,000 and even 400,000 people per month. Essentially, no job is safe, so you need a backup plan.

The wealthy very rarely rely on one source of income. Take a professional football player for example. They make millions from their day job and yet they still earn money on the side through sponsorships.

1.1 million people in the UK have a second job but as many as 25% claim to have a side hustle. We’re not proposing that anyone gets a second job on top of a full-time job but you may want to consider a side hustle.

One source of additional income that everyone should work on obtaining is investment income but realistically this is not going to be achieved overnight. Having multiple sources of income from your work is more easily achievable if you’re self-employed or a business owner.

Consider a website like Amazon which might be the ultimate example of income diversification. They are not reliant on any one customer, any one product, any one country, nor any one industry. What once was an online bookstore expanded into other physical products, and then into all manner of services, including music and video streaming, cloud services, financial services, logistics, and everything else.

On a much smaller scale, and so perhaps a little more relatable, a plumber will likely serve thousands of people in a small local area. No single customer will materially damage the plumber’s income if they choose to go elsewhere the next time their drain is blocked.

Multiple income streams are one of many advantages of being a self-employed plumber over being an employed office worker (other advantages being increased freedom, and greater control over their hourly rate). But the job with the single income stream is the one that the education system herds you towards.

You Need A Game Plan

A lot of people drift through life without a destination. They have no goals and therefore no plan. It’s little wonder why they don’t achieve much.

But if you want to accomplish great things – no matter how big or small – you need a game plan. You need to know how you’re going to cover your immediate living expenses, and simultaneously you need to have a long-term plan for achieving comfortable wealth, with a clear roadmap to how you are going to get there. Without a game plan, it’s just a pipe dream.

First things first, you need to draw up that budget. A lot of people find budgeting tedious but more times than not it’s because they don’t have a long-term game plan. Once you know what you’re striving towards budgeting becomes, dare we say it, fun.

People budget in different ways, but what we’ve found is if you overcomplicate it, you stop doing it. This is our tried and tested budgeting master plan:

- The day you get paid, transfer a pre-determined amount into a separate account, which will cover all your fixed bills for the month.

- Also on the day you get paid, transfer a pre-determined amount into a separate account, which is for irregular or non-monthly expenses. Christmas comes about once a year but from now on you budget for it monthly. Some excellent banking apps like Starling allow you to have separate pots all within the app. This budgeting method is often known as savings pots or the jam jar technique.

- Again, on the day you get paid, you transfer another sum of money to your investment platform. From your budgeting calculation you’ve already determined what you can afford or what is required to achieve your long-term plan. We call this pot our freedom fund and it’s so satisfying to watch it grow.

- Whatever’s remaining in your bank account is what you have to left spend during the month. If you find it’s not enough you need to go back and adjust your budget.

Only 30% of Americans, so presumably a similar number of Britons, have a long-term financial plan – no wonder most people are skint!

Insurance Matters – You Are Not Invincible

We reckon this could be one of the most overlooked parts of financial planning and we’ll admit it’s not something we even thought about until more recent years. I was always put off because the only time it was ever mentioned was when a seemingly dodgy financial broker was trying to push it, cos he clearly got some huge commission.

But as you go through your twenties you start noticing that nobody is invincible and sadly some people start falling ill; some even don’t make it. If you have loved ones that depend on you, you have a responsibility to ensure that in the case of your premature death they are financially taken care of. You do this by taking out life insurance.

The second type of insurance you should take out is Income Protection Insurance. This insurance product is designed to pay you an income if you are unable to work. Some policies will pay out for a few months, while others will pay out until you reach retirement age.

Unless you can somehow fund your lifestyle without income protection insurance, such as with investment income, we strongly urge you to take out a policy that pays out until retirement, which is exactly what we both did.

Because we feel so strongly about this, we’ve teamed up with the same broker that we both used, and if you visit our lifestyle insurance page you can read a little more and get a quote.

The System Isn’t Rigged

Some people who struggle financially blame the financial system, claiming that it’s rigged. But the fact of the matter is, just because they haven’t become financially successful doesn’t make it impossible. There are thousands of examples where normal people have become not just wealthy but insanely rich.

One such example is the rags to riches story of J.K. Rowling. You will know her as a best-selling author who has sold more than 500 million books and became a billionaire. But prior to her success she was desperately poor, jobless, and with a young child to provide for. She described her economic status as “poor as it is possible to be in modern Britain, without being homeless.”

Becoming a best-selling author might be difficult to relate to, so how about an incredible story about a janitor who secretly amassed an $8 million fortune by the time he died. He achieved this through smart spending and good investing habits, reports CNBC.

His family was “tremendously surprised” upon finding out about his hidden wealth. “He was a hard worker, but I don’t think anybody had an idea that he was a multimillionaire,” his stepson said.

There is no secret to becoming wealthy. It’s simply a case of adding value that other people are willing to pay for, spending less than you earn, and investing the rest. The more value you add, the more you will earn, and the more you can invest. Sooner or later, your invested money will be making more than you do. You can make as much money as you want if you are willing to put in the necessary work.

You Must Seek Out Pay Rises – They Won’t Come To You

Too many people moan that their employer doesn’t pay them enough, and yet they never seek out a pay rise. Your employer is running a business and their goal is to maximise profits for the shareholders, not to be handing out pay rises if they don’t need to. Pay rises aren’t given for nothing and certainly aren’t given to those who don’t reach out to take them.

Most employers will expect you to work a job for at least a few years before being eligible for a proper pay rise of more than a derisory 1 or 2 percent. So, to climb the career ladder at breakneck speed, the best thing you can do is to job-hop between companies. You’ll earn a promotion each and every time.

If you want to be paid more and stay at your current employer, you need to effectively tell your boss what the craic is, but this only works if you’re well-liked by the entire management chain. You’ll be amazed at how high up the chain your measly pay rise request goes to be authorised.

Your boss and your boss’s boss are unlikely to give you a promotion without first doing more than what you are already paid to do. You should literally ask your boss what you need to do to earn a promotion and then deliver that. At the very least, you make your boss aware of your desires and this will give you an idea of whether a promotion is even possible.

Start Investing For Your Future NOW

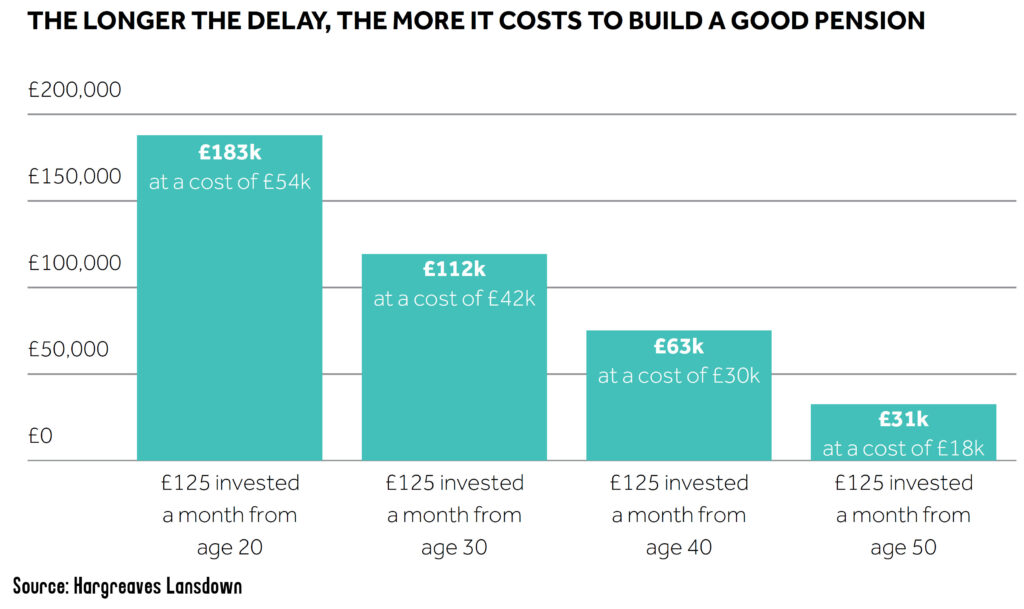

When it comes to investing, the earlier you start the better because compounding takes a very long time to make a serious impact! The longer you put it off the more you have to contribute to make up for the time you missed.

If you’re putting it off because you think your financial situation will get better, you’re taking a huge risk. From our experience, life gets more expensive as you get older, not cheaper.

If you invest £100 a month for 40 years from age 20 at 8% return, your pot is worth £324k at age 60.

But if you miss the first 10 years, and then invest £100 a month for 30 years, your pot is worth only £142k.

If you did start early, you might even be able to Coast FIRE if you wish. Coast FIRE is when you have enough in your investment accounts that without any additional contributions, your net worth will grow to support retirement at a traditional retirement age. For instance, stopping investing at age 40 and allowing your pot to grow by itself until you’re 60 and ready to retire. Then you can spend more money on lifestyle and enjoy your later career a bit more.

All your peers will be squirrelling away as much money as they can for the last couple of decades before they retire and probably still won’t have enough, whereas you who learnt these financial lessons early, could be coasting all the way to a comfortable retirement.

What other financial tips does everyone need to know before turning 30? Join the conversation in the comments below.

Written by Andy

Featured image credit: Dean Drobot/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday: