A handful of stocks have been flagged by my Stockopedia filters that I’ve felt compelled to buy – all big American household names.

With the market priced as highly as it is, we’ve been cautious in recent months about buying stocks. But while the S&P 500 seems crazily high right now it’s simply not true that the whole market is overpriced – there’s some genuine bargains out there on some brilliant companies.

In this video we’re deep diving into the fundamentals of 3 wicked stocks that I’ve just added to my portfolio. You can decide for yourself if you want to buy them too! Let’s check it out…

Written by Ben

💲💲💲 All offers listed on the MU Offers Page (including Stockopedia 25% discount & FREE trial, and FREE STOCKS from Freetrade and Stake).

👉 Best Investment Platforms page here.

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

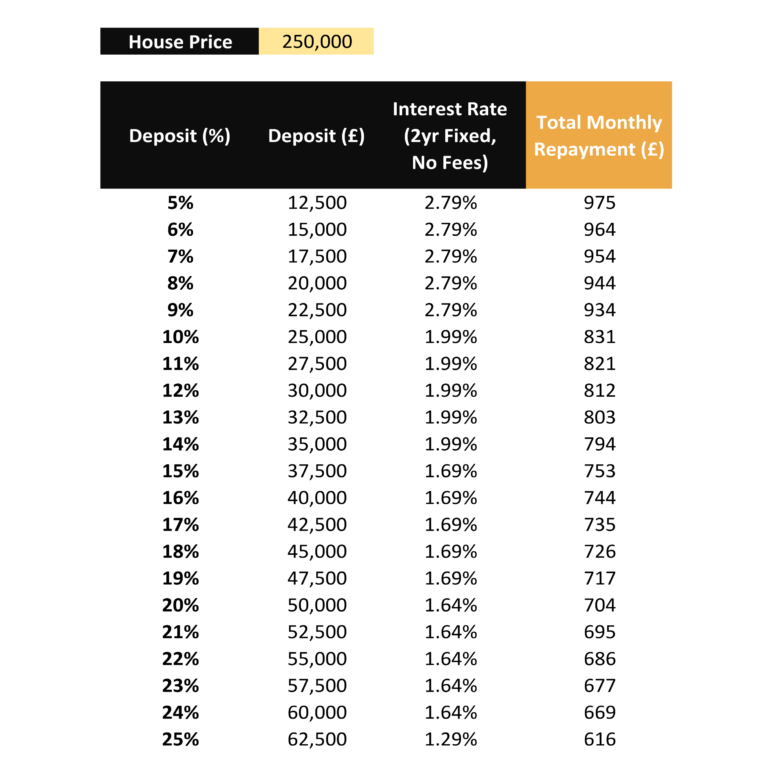

Whether you’re an aspiring first-time-buyer or are already on the housing ladder, it pays to know what the best mortgage deposit size is. That is, the optimal amount of cash to stump up upfront to buy a house.

Getting it right can make your house deposit one of the best investments you’ll ever make; and getting it wrong by overpaying can leave you much worse off than if you’d just put that money into your pension or ISA instead.

Not only that, but the range of possible mortgage types on the market can be totally overwhelming. Do you choose a lifetime tracker mortgage, or maybe a 3-year fixed? Should you get one with arrangement fees if it means the interest rate is lower? Is there an advantage to getting a 10-year term instead of a 30-year term?

In this post, we’ll be answering all of your mortgage questions, plus we’ll cover stuff you’ve never even thought to ask.

By the end, you should know what type of mortgage you need, and be confident that you’re making the right financial decision for you. Let’s check it out!

Are you wanting to buy a property to run as a Buy-To-Let investment, but don’t know where to start? Check out the Find Me A Property page, our property sourcing service finding the right property for your investment needs.

Investors have the option of having the whole process of sourcing, buying, and renting to tenants run for you, making the entire process as passive as it can get but still producing excellent investment returns of potentially 20%+.

For you the answer might be as simple as “whatever is the smallest amount I can get away with”, which with some lenders is 5%. We’re going to show soon just how big a mistake a 5% deposit is financially, if you can afford to put more down.

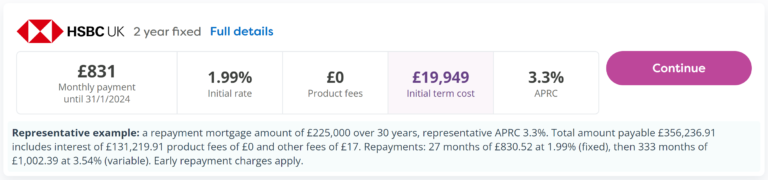

Assuming you can afford to pay a deposit exceeding 5%, let’s kick off by looking at the monthly repayments in the 5%-25% deposit size range:

The table shows the possible deposit sizes, the interest rates you’d be charged on the most popular products as of November 2021, and the money that would come out of your bank account each month, which includes interest and capital repayments – all on a hypothetical house worth £250,000, the UK’s average house price.

Comparing the monthly repayments are as far as most people get when deciding on a deposit size. They notice that a higher deposit means lower monthly repayments. There’s a quite a difference between 5% and 25%, with 25% deposits paying over a third less each month. So higher is better, right?

Not necessarily. For one thing, finding an extra £2,500 seems a lot of extra money to have to save up just to reduce your monthly bills by £10 (as in the case of moving from a 10% to an 11% deposit). And looking at the monthly repayments is far too simplistic a way to choose the optimal deposit size. Here’s what we’d do instead.

You need to think about your deposit as an investment and calculate the different rates of return for each deposit size in terms of how much mortgage interest it saves you from having to pay. It might then be obvious that chucking an extra £10k into your house deposit is not worth it financially.

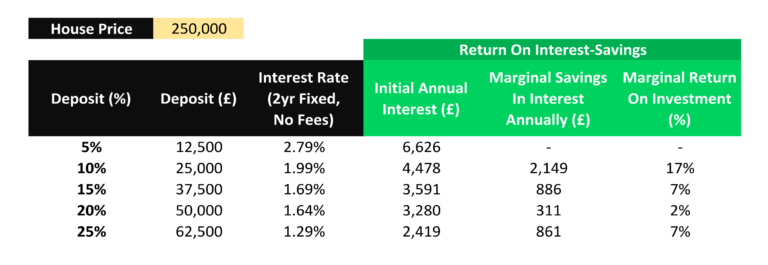

This table below looks at the marginal advantage of increasing your deposit size by 5% from one level to the next, in terms of Return On Investment. The interest rates that banks charge you move down in steps of 5% deposit sizes, so it makes sense to choose a deposit size in 5% increments.

A 10% deposit can get a 1.99% interest rate on a no-fee 2yr fixed rate mortgage. That’s a lot smaller than the best available rate on deposits between 5% and 9%, which is 2.79%. On a £250,000 house you’d save £2.1k in interest in Year 1 with a 10% deposit versus a 5% one. That is a 17% marginal rate of return on the extra £12,500 required.

A 17% return makes this likely to be the best investment you’ll ever make. If you can afford a 10% deposit, it’s therefore a no brainer. If you go higher than this to a 15% deposit, the extra £12,500 required will earn you a 7% return.

You might think it’s not worth the struggle to find an additional 5% deposit for a 7% marginal return on investment when you can get higher than this in the stock market. But remember – this is a guaranteed return.

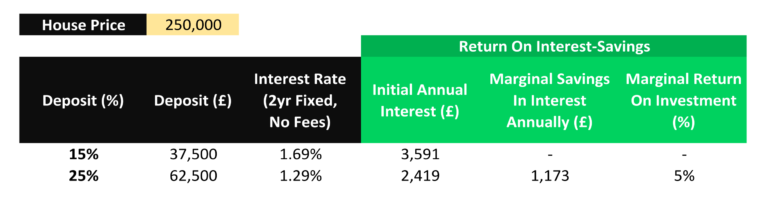

Our workings show that a 20% deposit is not a good decision – you’d be better off stopping at 15%, since a marginal 2% return can definitely be beaten by almost any other type of investment. But what about somewhere in between like a 16% deposit?

Going for 16% instead of 15% only saves you interest on the additional deposit money – so a tiddly 1.69%, the same as the interest rate. Whereas choosing 15% instead of 14% has a huge difference, because it brings down the interest charged on the entire borrowed amount from 1.99% to 1.69%.

A 20% deposit is a bad decision based on these interest rates, but 25% looks ok. The decision must therefore be between a 15% and a 25% deposit. If we compare the 2, the marginal return on investment from the extra deposit money is 5%:

But is it worth saving up an extra £25,000 just to get a 5% return on it, when you can get better by investing that capital elsewhere?

For example, that £25,000 could be invested into a Buy-To-Let property, that might make you a 20% annual return. Your money is still invested in the property market, just a different set of bricks to ones you’re living in.

Our overall conclusion is that it’s worth going for either a 10% or a 15% deposit on your home, but no higher – and nothing in-between!

Current homeowners should be aware that you can retrospectively reduce the deposit size in your mortgage when you next rearrange your mortgage deal – often called equity release. Read more here. It might make financial sense to free up cash that’s not really helping you save much interest and reset your equity to 15%.

You should carry this exercise out yourself on your own specific mortgage options, as our example looked at just one type of mortgage, a 2-year fixed. Let’s next look at the different types of mortgages you can choose from.

This is the first thing you’ll need to choose and will depend on your attitude to risk. Fixed rate mortgages lock in an interest rate for typically 2-15 years and are the most popular mortgage type.

After this you can easily swap provider to another deal, or else fall onto what’s called the Standard Variable Rate – a bad idea, since it’s typically very expensive.

With fixed rate mortgages you know what amount you’ll be paying each month, which is good for budgeting, and also means you won’t be hit if the Bank of England raises interest rates because yours are locked-in. However, the interest rate you pay is typically higher than the other options, since you need to pay for the lower risk.

In theory, variable mortgages are meant to have lower initial interest rates than fixed mortgages, but often they don’t – here’s a fixed and a variable that both charge the same.

Variable mortgages are higher risk than fixed, since the bank can change the interest rate as they like. A more transparent alternative to variable mortgages are tracker mortgages, which are still variable but vary strictly in line with the Bank Of England base rates, as opposed to the whims of your mortgage lender.

Tracker mortgages can be agreed for a period of time, say 2-5 years, and there are even lifetime tracker mortgages available. A lifetime tracker locks in your interest rate above the base rate for the entire life of your mortgage, usually without Early Repayment Charges. They can be more expensive though as you get so much flexibility.

Early Repayment Charges are large fees imposed on you if you want to change your mortgage deal within an introductory period. Examples of when you might need to do this are an unplanned house sale, or if you want to release equity.

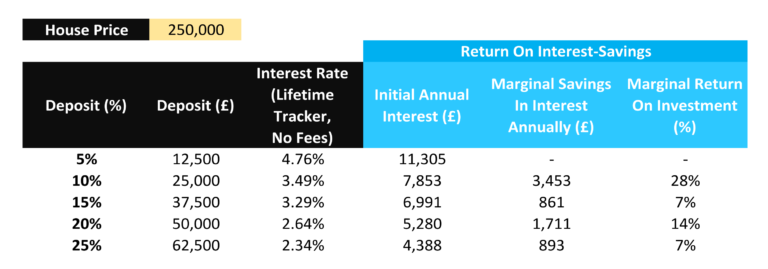

We also did the deposit size test on lifetime tracker mortgages and found that the interest rates were so high at the lower deposit levels that it made sense to go for a 20% or 25% deposit size:

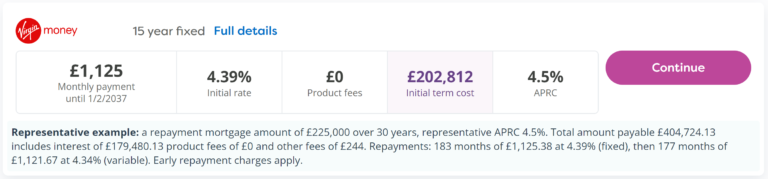

Most mortgages come with an initial term between 2 and 15 years. Using a fixed rate mortgage as an example, a 2-year fixed would lock-in an interest rate for 2 years, after which you’d be advised to rearrange your mortgage deal. But is it better to go for a short fix, or a long fix?

Short fixes of 2 years are better for those with an investor’s mindset, since the interest rates are lower due to the extra risk you take on by not knowing what interest rates will be like in 2 years’ time when you come to remortgage.

Here’s screenshots of a 2-year fix and a 15-year fix, each with a 10% deposit. The 15 year fix will cost you an extra £53,000 over the term, assuming rates stay the same – though rates likely will increase over the next 15 years:

Short fixes also mean you’re less likely to come foul of an Early Repayment Charge, as you can more easily work around life’s little surprises in a 2-year window.

I’d like to release a little equity from my house right now by switching provider, but I can’t without incurring a huge penalty because I’m locked into a 5-year fixed term.

Most mortgages on residential homes are repayment mortgages, and you don’t really have a choice in this except in special financial circumstances.

Interest-only are usually reserved for those in financial difficulty as an interim measure, or for the very wealthy with an approved future repayment plan in place. This is totally different to the situation with Buy-To-Let mortgages for investors, for which interest-only is the norm.

Repayment means you effectively make 2 payments a month, usually grouped together into one amount. One payment is the interest payment, determined by your interest rate. The other is to pay down the loan, determined by the length of the mortgage term.

Interest-only literally means you only make the interest payment – you do not pay off the loan.

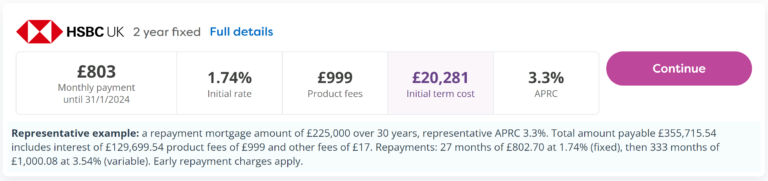

You’ll notice as you skim through price comparison sites that it’s a mixed bag of mortgages that charge either some product fees or none.

These are one-off mortgage arrangement fees, that are charged each time you arrange or rearrange your mortgage, which might be every couple of years if you choose to do 2-year fixed terms, for example.

You usually have the option of either paying them when you sign the deal or adding them onto the mortgage loan and dealing with them later.

This second option means you pay interest on the fees over the term of your mortgage, but the value of the fees themselves will depreciate against inflation over the decades, which may more or less offset the additional interest paid. On this logic, we would tend to add the fees to the loan.

What about those products that charge zero fees? Are they better?

Well, the ones that don’t charge fees tend to have a higher interest rate to compensate, so what you really need to look at is the total cost in the initial fixed period. Here, the one with the higher interest rate and zero fees has the lowest overall cost in the initial term:

Many providers now allow you to take out a mortgage over 40 years. This is significantly longer than what used to be available. 25-year mortgages used to be the norm. But is there an advantage to a longer mortgage term? Or is it better to set the term short, so you pay your mortgage off quicker?

It’s much better to go long. Taking a short term of say 10-years ties your hands, meaning you have to pay huge monthly payments or risk defaulting on your mortgage. While a long term means you can still make large overpayments if you choose to, but you don’t have to.

Many lenders charge you if you make overpayments of more than 10% of your initial mortgage balance, but that means you could get away with making overpayments of 10% for the first 10 years of a 40 year mortgage, fully paying off the loan and incurring no fees.

Therefore, it’s better to get a long-term mortgage, reduce your mandatory monthly payments, and overpay if you want to. But don’t feel the need to overpay!

Realise that a mortgage is amongst the cheapest and most manageable debt you will ever have, and approaching it with an investor’s mindset reveals how it might be better to put your excess cash instead into other, more profitable assets, like buy-to-let investing.

What type of mortgage do you think is best? Join the conversation in the comments below!

Written by Ben

Featured image credit: fasphotographic/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

Every study into the connection between wealth and health looks at it from the angle of how wealth impacts health – how being rich or poor affects your fitness and longevity. We want to know if it works the other way around too – does being physically fit and healthy improve your ability to make money? Do the statistics support this?

And if there is an element of cause and effect between getting fit and getting rich, is it due to you gaining increased money making abilities… or is it due to other people such as potential employers giving you more opportunities if you’re in good shape physically?

In this video we’re finding out if a good diet and regular exercise leads to financial rewards. Let’s check it out!

Talking of sport and exercise, if you want to increase your monthly income, why not try your hand at Matched Betting. It’s a step-by-step technique to profit from the free sports bets and incentives offered by bookmakers and could make you £500+ every month for less than an hour a day of effort. You don’t even need to know anything about sports, as bets are placed on both possible outcomes, for a guaranteed win. Check out our guides to find out more and for the latest offers.

Written by Ben

Featured image credit: Ollyy/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

Much has been made of the financial gap between the young and the old. From house prices, to rents, to taxes, to university fees, to the changing demographics of the country, and even the response to the pandemic – all seem uniquely designed to screw with young people.

In this post we’ll be laying out all the perceived ways in which Generation Z are being cheated by the system. Then we’re going to fact-check that narrative and see if there are any ways in which Gen Z is actually better off.

Finally, we’re going to look at the actions that you need to take NOW to avoid being one of those left-behind. Let’s check it out!

First up: Commission-free trading platform Stake (the go-to investing app to buy and sell US stocks) are giving away a FREE US stock worth up to $150 to everyone who signs up via this offer link and then funds their account with £50 or more within 24 hours. Don’t forget to claim yours!

The biggest planned shake-up of planning laws for 70 years has just been abandoned after a backlash from government backbenchers and their older home-owning voters. Reforms designed to help hit a target of 300,000 new homes annually by the middle of the decade will be watered down.

Planning reform is just one solution to the housing crisis that’s causing misery to so many young people who are unable to afford their own home. When reforms like this are cancelled it just compounds the problem.

Where 19% of 25-to-34-year-olds were private renters in 1997, that figure was 44% in 2017. And those aged 35-to-44 are three times more likely to be renters than they were 20 years ago.

Another problem with housing is that there isn’t enough stock of good, 4-bed-plus family houses.

The blame for this is often laid at the feet of the old, who continue to live in castles too big for their needs after their kids leave home, while young families are forced to live in new-build cardboard boxes.

But the true fault lies with the government. Their stamp duty tax on house purchases actively punishes people who choose to downsize.

An older couple choosing to help out the younger generations by moving out of their £500,000 4-bed house into a £350,000 2-bed face an immediate stamp duty tax payment of £7,500. It’s not surprising that they choose not to do this. The tax system is therefore structured to limit the availability of family houses for young people.

Regarding rising house prices and rent prices, are they ever going to stop? A decent-ish 2-bed flat in Birmingham rents for around £1,000 a month. How can a small cube in an apartment block cost so much?

The situation is echoed across the country, with people forced to pay ridiculous prices for substandard living conditions.

At our age, our parents’ generation were all about 10 years into paying off their mortgages on big houses.

Fact Check

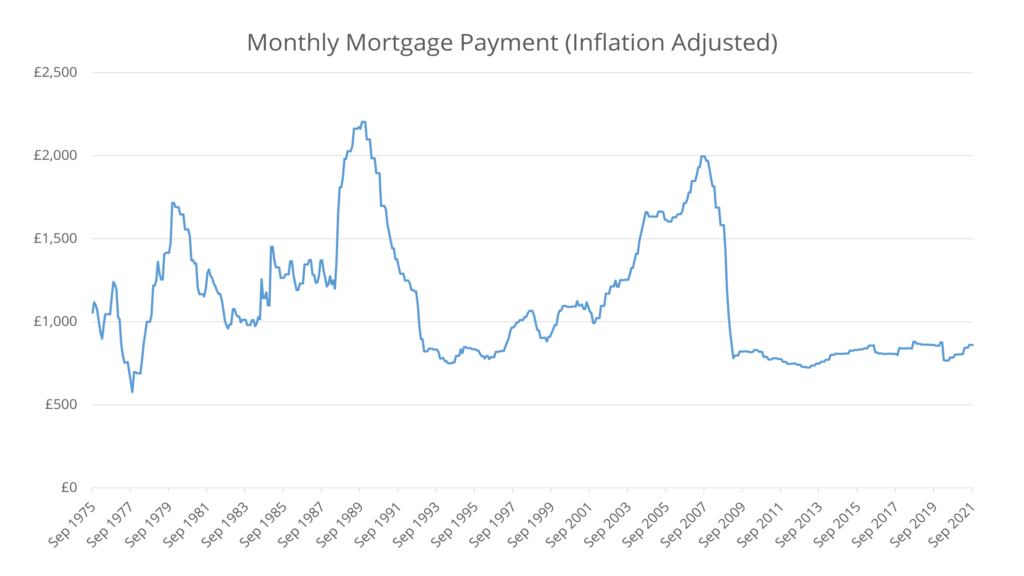

Which really matters – house prices, or how much your mortgage payment is each month? The fact is that interest rates were much, much higher in the past.

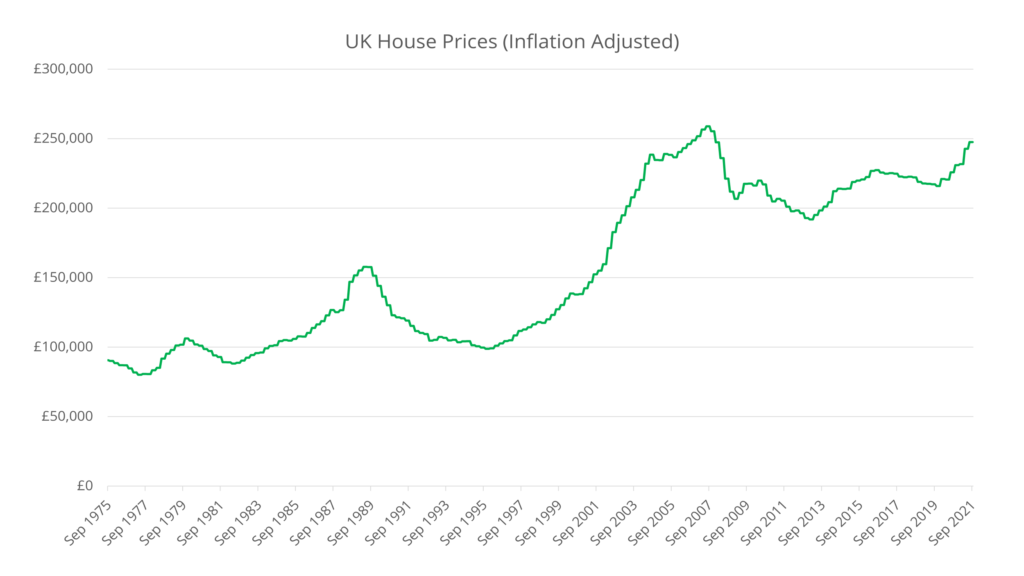

We’ve taken the inflation adjusted average house prices going back to the 1970s, and worked out from the Bank of England base rate in each of those years roughly how much a family would be paying for their monthly mortgage, in today’s value of money:

Surprisingly, the current generation is living in one of the BEST times to buy a house, in terms of affordability, thanks to record low interest rates since the 2008 financial crash. People in the 80s, 90s and early 2000s had it much, much worse.

And looking next at the inflation adjusted house prices in isolation, though Gen Z really does have a deposit problem, it’s not a unique one – equivalent inflation adjusted prices were previously seen in the years before the financial crash:

Young people don’t seem as annoyed as they should be about ever-rising taxes – those who came before them didn’t have to pay anywhere near so much.

The tax burden right now is the highest it’s been since 1948, at 35.5% of GDP, and it’s expected to rise further before the next election. The trajectory since the 90s has been a steady upwards climb, and the government has big spending plans for the next decade that will need more taxes to pay for them, such as going green and ‘levelling-up’.

Tax is paid predominantly by those of working age. Pensioners, who are the ones who actually vote, tend not to tolerate big tax rises on their wealth.

Indeed, in a policy representative of the age divide, the government is hiking National Insurance taxes on younger, asset-poor workers so that the social care of older, asset-rich people can be funded without those retirees having to part with their wealth or insure themselves against the costs of care.

As the Resolution Foundation noted, ‘a typical 25-year-old today will pay an extra £12,600 over their working lives from the employee part of the tax rise alone, compared to nothing for most pensioners’. Pension income will not be subject to the levy.

You can double this hit when you factor in that Employers NI has gone up too by the same amount – an indirect tax on your future wage potential.

Fact Check

A counter argument in favour of the elderly holding onto their assets would be that those assets will eventually be passed on to Gen Z through inheritance. Indeed, inheritance may now be the only viable way that the average Gen Z-er can scrape together a house deposit.

But obviously, not everyone stands to inherit so you still have to question how fair this is.

University has been devalued as an institution. It used to be that only the brightest young minds went to university, and those who went found that it transformed their fortunes.

Now, everyone and his dog has a degree. People working on the checkouts in supermarkets have degrees. Degrees are increasingly worthless. It’s work experience that gets people the best jobs – not degrees alone.

But you still have to go to uni to be on a level playing field with your peers. You have to spend 3 years racking up £50,000 in student loan debt to get a basic job.

This generation is unique in that they almost have to be saddled with debt (which they’ll never pay off) just to get the minimum wage.

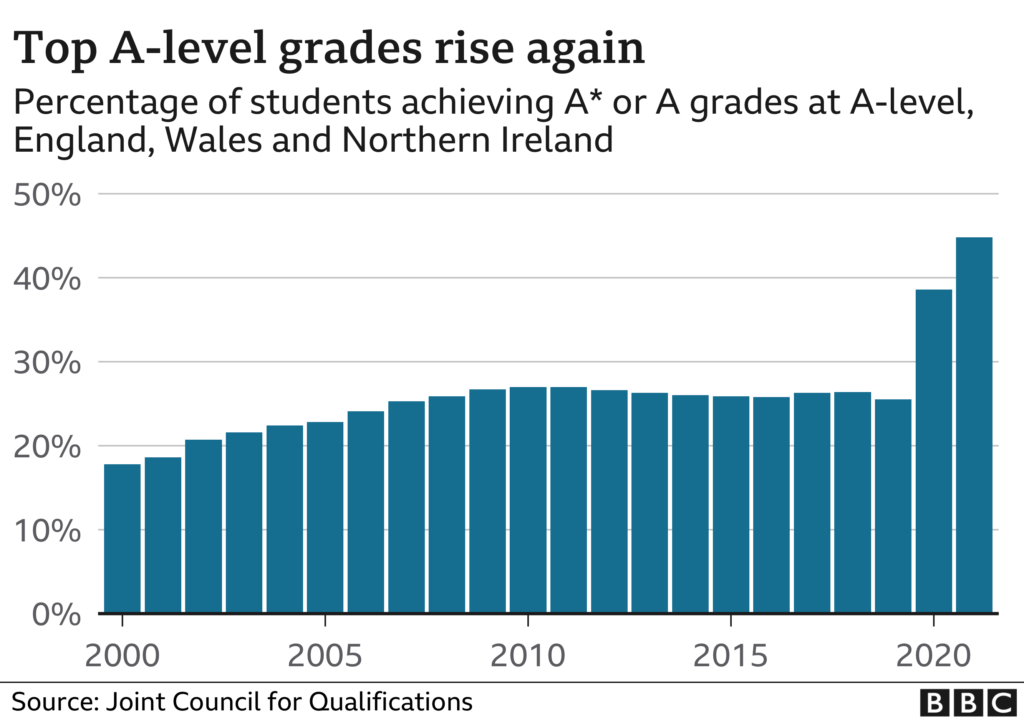

Young people suffered the worst financially from the lockdowns in terms of opportunities lost, damaged education, and careers interrupted – the current batch of school and college leavers have had a particularly rough couple of years.

Not only has their learning been disrupted but many of them have been given top grades as no exams were taken – damaging trust in the grading system:

Genuinely clever kids have the same top grades as kids who in other circumstances would have got lower grades. Will they unfairly miss out on places at the top universities as a result of the increased competition?

An obvious issue is student loans, which never existed in the modern form for previous generations. University even used to be free.

There’s no denying that university fees are high, but we don’t believe student loans are as damaging to your finances as they appear to be.

Fact Check

Student loans aren’t really loans: they’re a tax on your income that you only pay if you get a high enough salary, currently taxed at 9% on any income earned over £27k for Plan 2. That “debt” you think is weighing you down isn’t really doing anything of the sort.

The alternative to this student tax used to be to force the whole country to pay for your degree through higher income taxes.

Whether asking 20-year-old cleaners to pay the university fees of 20-year-old students through higher taxes is fair or not will depend on how you think a tax system should be run. There’s an argument that everyone benefits from having an educated population. We ourselves are split on the subject. Either way, the taxpayers would be footing the bill – the question is whether it should be just those with degrees paying that tax, or everyone.

Mass immigration since the 1990s has pushed down wages in the UK. It’s simple supply and demand economics.

There was an almost infinite pool of people willing to take a limited number of jobs in the UK. That’s why you see office workers on close to the minimum wage, and why nobody wanted to be a delivery driver before the current food and fuel crisis. This has made it difficult for Millennials and Gen Z to earn good money from good careers.

Fact Check

Whether due to Brexit, or the knock-on effects of Covid travel restrictions, or both, there are signs that low wages are starting to improve in certain sectors, like truck drivers and brickies. But for as long as there are skilled social care nurses on low wages, the problem won’t have gone away.

Despite a few positive signs, we think it’s fair to say that Gen Z is the first generation in a long time to be worse off than the generation that came before them.

Given this, it’s crucial that young people take extra steps that their parents and grandparents didn’t have to.

To address your immediate money issues, you need to stop what you’re doing and reflect on your career. Do you need a better paid job or even a complete career change?

Could starting a business pay better than what you’re making now? One advantage of working for yourself is that you don’t have to split the profits of your labours with an employer.

Or could you top up your job income with a side hustle? Check out our matched betting guides for just one way to make extra money on the side for just a few hours a week.

Something you must do is get a firm understanding of your pensions. Previous generations more or less had their retirements handed to them – you must work harder for yours.

Too many people are contributing too little to their pensions. The rule of thumb is that someone starting saving at age 20 should be putting aside 10% for the rest of their working career. Fall behind and you’ll have to pay much more later!

Where you invest your pension matters too. We’ve shown in this previous video how UK workplace pensions are geared towards underperforming investments, often with too little investment risk taken on the part of young people. The result is a mediocre growth rate and much smaller pension pot. We show you in that video how to take control of your own pension funds.

Perhaps even more important than your pension is that you get on the housing ladder a.s.a.p, unless you’re happy to rent forever. With house prices growing ever higher, you’re only going to be left further and further behind the longer you fail to prioritise this goal.

If that means cutting back on the new car until you’ve built that house deposit, so be it.

If you know you won’t be able to afford a house for years to come, a good alternative would be putting your savings into investments like stock market funds and gold to protect against inflation. Those with houses already should be doing this too.

Houses, stocks and gold are financial assets, in the sense that their prices generally go up. Everyone who doesn’t own assets will be left behind financially in the years to come. Those who own assets will be swimming with the tide of inflation rather than against it.

Do you think Gen Z is being cheated? Join the conversation in the comments below!

Written by Ben

Featured image credit: View Apart/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

Hey guys, in this post we’re going to be looking at some of the really common personal finance misconceptions that many people believe to be true. Some of these misunderstandings could be very damaging to your finances, so let’s set the record straight today. Let’s check it out…

As always don’t forget to grab your free stocks and free money when you sign up to any of a number of investing platforms and financial services. Check out the Money Unshackled Offers page for info.

Everyone moans when the government has their hand in their pocket but it’s evident that many people don’t actually understand the tax system. Worryingly, some people believe that if they earn more money before tax, when they enter into a more expensive tax bracket, they’ll actually take home less.

The misconception is that when you earn over a certain amount and become a higher-rate taxpayer paying 40%, then this tax rate would apply to all your earnings. This is not true in the slightest.

In the UK we use a progressive tax system, meaning taxpayers will pay the lowest rate of tax on the first level of taxable income in their bracket, a higher rate on the next level, and so on.

For example, Max earns £60,000 a year. He gets the personal allowance of £12,570, which is tax-free. The 20% tax bracket currently applies to earnings between £12,570 to £50,270 or in other words the first £37,700 that exceeds the personal allowance. That means Max gets taxed at 20% on £37,700 and 40% on the next £9,730 earned.

For those who aren’t as fond with numbers as we are you can bang earnings into tax calculator, like the one at thesalarycalculator.co.uk, and it will tell you the amount of tax that will be paid.

Even if you don’t fully understand the numbers, it’s important to understand how the tax brackets are applied. Some people are even avoiding overtime or promotions because they think it will cause them to take home less.

If you’ve seen our videos or posts before when we’ve stated that’s it’s not worth working more, generally we mean that after income tax, NI, pension, and student loan deductions, the money earned is too small to be worth our limited and precious free time for the extra effort. But crucially, that overtime would result in more take-home pay.

According to hitched.co.uk the average cost of a UK wedding is £32,000. They surveyed over 2,800 couples to get to that eye-watering number. As someone who values their free time so highly, I cannot understand how that is the average cost of a wedding in the UK, which would take years of hard graft in order to save up for.

We reckon a couple could travel the world for more than a year and still have change to spare – some could probably travel for a few years on that budget and have the time of their life.

Alternatively, that’s a sizable deposit that could have gone towards their dream home. Or for those that want to set themselves free that is a very good-looking retirement pot that could easily grow to be worth more than £100,000 in just 25 years. And as for those taking on debt to get married… tut tut.

wedding expenses")

Above are the top 10 expenses for the average wedding. £5.4k is spent on the venue, £4.6k on the honeymoon, £3.9k on food and another £1.6k on drink. Then you have huge amounts on the ring, dresses, photography, and on and on it goes.

Money Saving Expert have a useful article giving tips on how to slash the cost. We won’t repeat it all here, but one interesting point is that you can get an all-in wedding reception for £4,500 … at Wetherspoon’s. It includes a three-course meal with wine for 100 people, a DJ, decorations and a wedding planner. And apparently this isn’t just any Wetherspoons, it’s a swanky pub in the heart of central London.

Fair enough that might not be to your taste, but the point is that there are loads of stories of people getting married on the cheap – and in many cases for even less than the cost of a swanky Wetherspoons reception.

As someone who doesn’t particularly care for weddings, before even spending a penny I’d encourage you to first consider whether you’re getting married because everyone else does or whether you actually want it. Sounds obvious but many people are too busy going through the motions and following society’s life plan that they never consider what they actually want.

This is a two-pronged misconception. Many people believe that they cannot retire until they are at least 65 when they qualify for the state pension – and also that they will need to top this up with a workplace pension, which they assume to be the only way to privately save for retirement.

Our regular viewers who have a keen interest in investing will know this is not true at all. You can retire whatever age you please and this could be 20, 30, or even 40 years before the state dictated retirement age.

The state pension dates back to 1908 and was originally reserved for those who were 70 but back then life expectancy was short. Only 24% of people reached State Pension Age and of those the average life expectancy was a further 9 years. Basically, the government was paying barely anything out.

Fast forward to today and people are drawing on the state pension for 20+ years, which is a huge and possibly unsustainable burden for the government. The state pension cannot be relied on still being around to fund your retirement when you get to your 60s.

You must save for retirement privately and if you use the right savings vehicles, you can start drawing down on your retirement pot at whatever age you like. The only caveat is you must build it big enough to out survive you.

Anecdotally, most people give no consideration to retirement planning other than saving into a matched contribution workplace pension. In the rare cases of having a good salary and a generous employer making big contributions this could be quite a chunky pension that allows you to retire in your mid to late 50’s, which is the earliest a pension can be accessed. Unfortunately, for everyone else, retiring in your mid 50’s is unlikely unless you actively plan for your retirement.

Crucially, you can retire even younger than this if you prioritise your future and utilise a variety of other wealth building tools. Someone that saves £500 a month for 30 years could quite easily have a retirement pot in today’s value of money worth £600k, allowing a 20-year-old to retire at 50. This can be done using a combination of a pension and a Stocks and Shares ISA, which allows you to access the money at any age.

Another powerful retirement wealth builder is buy-to-let property and there are no limitations in what age you can access any income that it generates, nor any restrictions of when you can sell the properties to release your wealth. Obviously buy-to-let property is not easy if you do it all yourself, but the gains can be life-changing.

Check out this post next if you want to see a worked example of how much profit property can produce by having someone else do all the work for you and find out how you can get help starting to invest.

One further way we’re growing our wealth fast is the use of spread betting to invest in S&P 500 futures. Here we explain exactly what we’re doing. Very briefly, we’re using leverage to earn mega tax-free returns that can be accessed with no age restrictions. It’s a super complicated subject, so tread carefully with this one.

Whenever you buy something that you want are you guilty of always buying new? There’s a misconception that used items are old, tired, and trampy. Hands up, for most items I’m guilty of overpaying just to get my hands on a needlessly brand-new item.

But there are numerous times when buying used items gets you almost as good of a purchase as new ones, but for significant cost savings. The most obvious one is a car. Some used cars are in such good nick that they still have that new car smell.

Other items where old is almost better than new include exercise equipment. Many people buy these items with the intention of starting a get fit and healthy regime but fall off quickly and then try to unload these bulky goods that take up too much room. You can then snap up a bargain!

With items like dumbbells, you can even resell later for a similar price to what you paid on the second-hand market, so they effectively cost you nothing during the time you owned them.

Many things that your kids need can also be bought used for considerable cost savings, especially when your kids are far too young to even notice or care. A brand-new pram can cost hundreds or even thousands of pounds but buy used and it can cost less than £50. Trust us, your kid(s) won’t even notice.

Used furniture is another huge cost saver. I’ve cleared a few things recently to make room and have been selling them at almost giveaway prices, for items that are in close to perfect condition. Understandably, for those of you like me who are still a little snobbish when it comes to new items, maybe you can buy used for things you won’t use that often. Outdoor furniture is a prime example of something that you will only use twice a year, but you can save a small fortune by buying used.

New build homes are also often worse than older homes. Forget the new-build premium, which is another problem – we’re talking about build quality here.

Properties these days are thrown up in no time with poor quality workmanship and corner-cutting. They are also super stingy with space, trying to pass off cupboards as double bedrooms. Older properties – even those built just 15 years ago – are usually far bigger with additional space for stuff that is often overlooked when you’re shopping around; things like storage space.

The average person on the street – and the government, and the banks – thinks a high income from a job means you are wealthy, but there is fundamental difference between income and wealth. Wealth – when managed right – should be permanent savings. But salary income is the money you earn and often disappears as fast as it comes in.

A smart person will slowly turn income into wealth by investing wisely over time. Conversely, a dumb person with wealth will run it down to zero.

Wealth is how much assets you have. For example, a pensioner living in a house valued at £1 million is wealthy, even though her pension brings in a tiny income of just £100 a week.

Moreover, not all wealth is the same. In our example, although our pensioner has £1 million in wealth it is in an unproductive asset meaning it’s not producing any income. Income generating wealth is superior and includes the likes of businesses that you own and investments you have.

People tend to be interested in how much another person earns in their job but cares less about their wealth. It should be the other way around.

Someone who earns £100k a year from their job but blows the lot will work every day until they die. But someone who has financial wealth of £500k held in productive assets and only lives on the £20k a year generated from their investments theoretically never needs to work another day in their life.

Furthermore, a high wage income can be taken away from you at any moment. You could lose your job and may find it impossible to get another paying anywhere near the same. This frequently occurs in older age.

Most professionals should expect their pay to peak between the ages of 40 and 49, according to earnings data from the ONS, while salaries fall to their lowest level during their 50s. Or to put it more succinctly, you have got to turn income into wealth before it’s too late!

What personal finance misconceptions do you think are most common? Join the conversation in the comments below.

Written by Andy

Featured image credit: Ivelin Radkov/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

Hello and welcome to Money Unshackled News. The headlines:

We’ve gathered all the latest money news from the past few weeks that matter most to your finances. If you find this financial news bulletin useful then hit the like button and let us know down in the comments. Let’s check it out…

If you want to grab some free cash check out the Offers page. InvestEngine, Loanpad, EasyMoney, Octopus Energy, and others are all giving away £50 in welcome bonuses. Free stocks available too.

The Bank of England holds interest rates at an all-time low of 0.1%, despite widespread anticipation it would increase the rate to 0.25%. The Monetary Policy Committee voted by a majority of 7-2 to maintain the Bank rate as it is.

Analysts have said that they expect the rate to be hiked to pre-pandemic levels in the next 18 months as the economy resumes a more steady course.

Governor Andrew Bailey fought back amid suggestions that the Bank wrong-footed investors by signalling an imminent rate rise ahead of the decision and told Sky News: “It was a very close call”.

Lenders Natwest, Lloyds and Barclays – whose profitability tends to be boosted by higher rates – saw their shares fall by 4% or more as a result of the news.

Mr Bailey told Sky News that rate-setters still needed to see “hard evidence” on the state of the jobs market before any hike and that an increase would not directly address supply chain issues that are key causes of the acceleration in price rises.

In related news the UK is facing a cost-of-living squeeze after the Bank of England predicted that inflation will be heading to 5% early next year, its highest level in a decade.

Our take on the matter is that it’s only a matter of time before the decision is made to slowly begin to start raising the interest rate but as stated many times before we cannot see this increasing much due to the financial struggles that both Britons and the government are facing.

The Budget slipped by largely unnoticed in October, as for once it seemed that taxpayers, savers and investors had managed to avoid the usual punishment beatings.

But a little reported tweak to pension rules slipped though the net which may have big consequences for those of you saving for retirement. Workplace pensions currently have a fee cap in place which stops your fund provider from fleecing you for fees. This Budget paves the way for this cap to be removed.

Martin Lewis says: “This can be positive, as it allows a wider choice, but must not be allowed to push up the norm for charges for simple funds.” And if you’ve looked at your workplace pension, the fees on funds can be pretty steep already.

A half solution might be to at least move old workplace pensions to a SIPP where you can pick your own low-cost funds; more information on SIPPs can be found here and includes welcome offers for some providers. But if you want your employer to match your contributions, you’ll likely have to stick with the more expensive workplace pension.

JPMorgan says Ethereum is a better bet than Bitcoin as interest rates rise, due to the boom in DeFi and NFTs. Ethereum is at the heart of decentralized finance and the market for non-fungible tokens, two booming areas. Bitcoin is apparently more akin to digital gold, which is likely to fare less well as interest rates and bond yields rise.

JPMorgan analysts, said in a recent report that rising interest rates could pose a problem for Bitcoin, just as they traditionally do for gold. “With Ethereum deriving its value from its applications, ranging from DeFi to gaming to NFTs and stablecoins, it appears less susceptible than Bitcoin to higher real yields.”

The bank’s analysts also said Ethereum may be the better bet over the longer-term due to the growing importance of environmental concerns in investing.

Both cryptocurrencies currently use a validation and security system that uses vast amounts of electricity. Yet Ethereum plans to move away from this system to a far less energy-intensive one by the end of 2022.

However, JPMorgan has said that both cryptocurrencies currently appear overvalued since most institutional investors won’t touch them due to being far too volatile.

Honestly, we have no idea how anyone can attempt to value any crypto at this early stage in their lives. Who would seriously be surprised if Bitcoin or Ethereum tripled in value from here, or collapsed threefold? Much of their value depends on their always being someone else willing to buy the coins.

Could either follow the path of SQUID coin, a cryptocurrency designed around popular Netflix show Squid Game, which rocketed 23 million percent in value to $2,860 a coin… only to plummet to nearly $0, when investors found no-one else was waiting in the wings to buy their coins.

Now for something you’ll never see on the telly – some positive news! The number of people shopping on Britain’s high streets in October beat all major economies in the European Union new data has shown, reports Yahoo Finance.

Total UK footfall saw a 3.2 percentage point improvement in October compared with the month before, boosted by the school half-term and Halloween.

However, it’s still down 13.7% compared to this time 2 years ago – i.e., if we compare it to the October before the pandemic.

We may have lost the Euros to Italy back in the summer but we’re smashing their retail figures; Italy’s footfall was down 34.6%. Similar dire figures were seen for Spain, down almost a fifth; Germany slumped 26.2%; and France declined 34.9%.

The Sun reports that Christmas shoppers will spend a record £85bn as eager families are already hitting high streets for presents and food. Brits are expected to splurge over £5 billion more than last year’s £80bn Christmas shopping bill. Money saving website VoucherCodes says the average Brit will spend nearly £1,300 per person for the special day.

A massive global crypto fraud which began in China has recently spread to the US and Europe. The Sun reports that a guy lost $60,000 in a new crypto scam when a dating site fraudster brainwashed him into investing in a fake scheme. This unfortunate guy is one of thousands who have fallen victim to the scam.

The fraud is known as sha zhu pan – or “pig butchering”- in a sick reference to how the target is said to be “fattened up” ready for slaughter. It sees professional con artists linked to the Chinese mafia spend months building victims’ trust before pushing them to invest in bogus get-rich-quick schemes.

The guy bought some Ethereum via an online broker she recommended. The clever part of the scam is that the victim initially makes a profit and is even able to withdraw the money – but by then they are hooked. Sha zhu pan has been huge in China in recent years but was virtually unknown in the West until this year.

The scam focuses on tech-savvy young professionals with an interest in cryptocurrencies. This could include many of our audience, so stay vigilant. It’s probably similar to the scammers that are always clogging up the comments section below our and other Finance YouTubers’ videos, so be wary of YouTube comments about crypto too!

Lloyds Bank is to shut 48 branches amid a decline in customer visits. Similar stories to this have been hitting the headlines for years now, so should come as no surprise. But what may surprise you is the rate of closure. Financial analysis firm AskTraders said high street banks will disappear completely from the UK by April 2032 if the current rate of closures continues.

Just 7,655 banks remain on British high streets, with an average of 55 banks closing every month for the past five years – that’s 660 a year.

While the loss of a useful service and jobs is quite sad, honestly when was the last time you actually visited a bank branch? Anecdotally, people we’ve spoke to who say they occasionally use a bank to pay in a cheque had no idea that most good banks allow you to pay in cheques using their mobile app by simply taking a photo.

Of course, closure of banks will hurt some people more than others. Trade union Unite said “These closures will deny access to vital services and cash to thousands of customers who will be disadvantaged as a result.”

But the fact of the matter is that society is increasingly moving towards being cashless and online, so surely banks cannot incur massive costs to please a small percentage of people? Moreover, most people are unaware that basic banking services for your bank are likely accessible via the Post Office, which are usually present in every town in the country.

Is going green such a good idea? While most will answer yes and say it’s of vital importance, the cost is set to be astronomical. Downing Street has set out its plan to cut carbon emissions to net-zero by 2050, and the inflation adjusted cost of doing this is expected to be £1.4 trillion over the next 30 years, the Office for Budget Responsibility has warned. That’s the equivalent of £1,700 a year for the average household, on top of £3,000 of tax increases per household already announced over the last year.

Phasing out gas boilers over the next decade and investing in home insulation, electric car charging points, and nuclear power plants are all part of Boris Johnson’s vision for ‘Green Britain’. We are yet to be given an exact breakdown of how costs will be spread, but higher taxes and higher consumer prices are expected to contribute to the total sum.

Replacing boilers with low-carbon electric heat pumps is expected to cost £10,000 on average and not everyone will benefit from a voucher scheme which covers half that sum.

The Telegraph reports that less than half the population is willing to pay thousands of pounds to make their homes greener and help meet Boris Johnson’s net zero goals.

And finally in property news, half of borrowers will still have a mortgage when they are aged 65 and over, reports whatmortgage.co.uk. Increasing numbers of people are borrowing with mortgages in their later life leading to concerns the dream of retirement may be under threat for many.

UK Finance said: “There’s been growing demand for mortgages from those aged over 55 and this is set to continue as more people live and work for longer.” For the average person this is a very worrying sign. The ability to work past your sixties should not be taken for granted. Ill health leaving you unable to work and unable to fund your mortgage repayments in retirement is a real threat.

For the investors watching, you may actually prefer to still have an outstanding mortgage in old age because you might be willing to tolerate the risk of borrowing on a cheap mortgage to invest and earn greater returns elsewhere. This is something we ourselves might plan to do if we’re not already loaded at this point!

What’s your opinion on higher consumer prices and higher taxes to fund green policies? Join the conversation in the comments below.

Written by Andy

Featured image credit: Vitalii Vodolazskyi/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

We’ve talked before about the incredible returns you can get from owning rental property in the UK. What we want to talk about today is that if you wanted to invest in property, paying to outsource all tasks to do with sourcing, owning and managing them doesn’t really harm your wealth – and may even increase it.

Too often property investors think they have to be active landlords, doing everything themselves. They manage the tenants, fix the toilets, and find their own properties with no surveying or construction knowledge, often resulting in expensive problems down the line.

Meanwhile, if you’re willing to outsource every task, it means that all you need to become a property investor is money, and a basic grasp of the finances. It doesn’t even matter if you don’t live near the property.

Being a landlord is a job. We’re saying, don’t be a landlord – be a property investor!

In this article we’re going to run you through an example rental property for sale right now in Manchester, and show you the expected income, costs, and Return On Investment with it being run as an outsourced investment, versus a self-managed one.

You might be surprised how little difference it makes to your wealth, compared to the time you get back – time that you could put to better use making money elsewhere!

Be sure to check out the new Find Me A Property service for those wanting our help with buying rental property.

An investment should not require much of your time in order for it to grow. The advantage of an investment like a stock market fund is that you can set it up and forget about it, and return in 30 years’ time to see how it did.

Most property investors meanwhile put way too much time into bleeding their assets for every penny of possible return – they’re tempted to micromanage because they have full control over the asset and are reluctant to spend any money.

Many fancy apps and websites have popped up to make investing in property more passive by pooling investors’ money together into funds, but they are no substitute for the magnified returns possible by actually owning physical buy-to-let property yourself with a buy-to-let mortgage. And, the assumption that buy-to-let property cannot be completely passive is wrong.

Let’s start with a real-world example of an investment-grade house that’s on the market right now.

On paper, it ticks all the boxes for me in terms of location, size, price to rent ratio, and condition, but I would visit it first to make sure. If you wouldn’t have a clue how to find the right property, remember, you can outsource everything – even that.

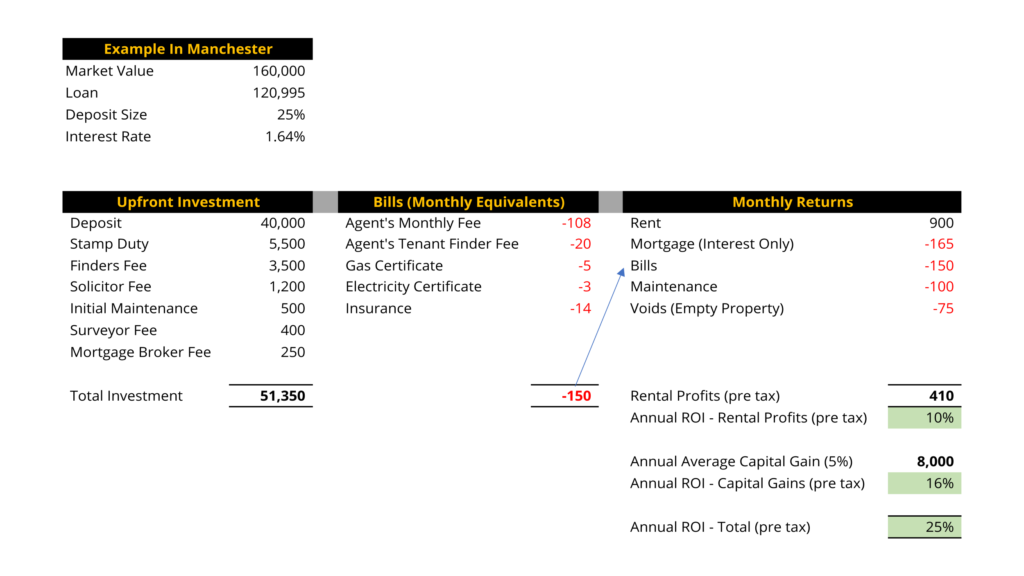

Below are the numbers for this particular investment, starting with the house price and the mortgage. We’ve found Natwest and RBS mortgages offering a rate of just 1.64% on a 25% deposit, which is the industry standard deposit size for buy-to-let mortgages. The mortgages have a £995 fee, which you can just add to the loan instead of paying upfront.

Next is the breakdown of what you’d actually pay for this opportunity (Upfront Investment column), having outsourced all the jobs of finding and purchasing the house to professionals. The vast majority of the upfront investment is the required deposit. The rest is all set-up costs that you must factor in to work out your true return. If this looks a lot to you, we’ll look at what you can do about that shortly.

Then there’s the monthly bills you’d expect to pay (Bills column), which assumes an agent fee of 12% on the rent, the once-in-a-blue-moon agent’s fee for finding new tenants shown as a monthly equivalent, and monthly equivalents for safety certificates and insurance.

The bills feed into your Monthly Returns calculation. Rental income is expected to be a healthy £900 a month on this property, and knocking off amounts for mortgage interest payments, bills, maintenance and void periods, you get a pre-tax rental profit of £410 a month. Annually, that’s a 10% Return On Investment against the £51,350 original investment.

But rental profit isn’t everything – you also expect to get a sizeable capital gain. Assuming your £160,000 property will be worth £168,000 in 1 years’ time, based on a historic 5% average growth rate, that £8,000 gain is an additional 16% Return On Investment. Overall, despite not being a hands-on landlord, you’re making a 25% pre-tax ROI.

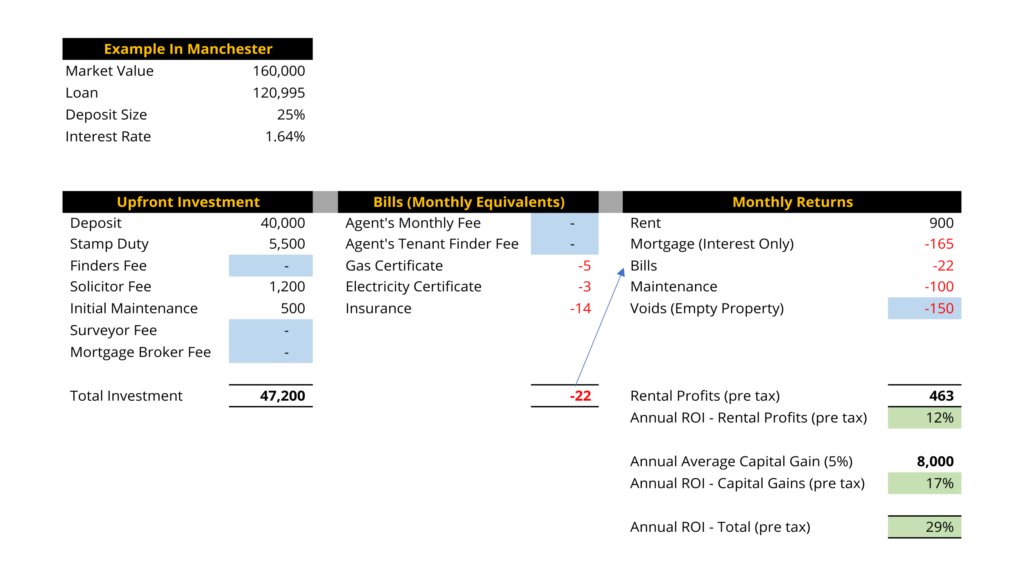

A 25% ROI is pretty tasty, and that’s based on the premise that you’ve taken out all of the nasty time consuming work from being a rental property owner. Let’s quickly add that time and effort back into the equation and see what difference it makes to your ROI:

The blue cells are the costs associated with outsourcing that you can change. Let’s set the upfront outsourcing and the monthly agent’s fees to zero and see where that leaves you.

We’d also expect voids to increase if you were doing it yourself, from maybe 1 month a year to 2 months a year, since professional agents will likely do a better job of finding and retaining good long-term tenants – it’s what they do.

Your ROI has increased by doing everything yourself, from 25% to 29%. There’s hardly any difference – both are epic returns! The question you need to ask yourself is whether that 4% difference is worth giving yourself a second job over?

As a remote hands-off investor, you’re going to need to outsource a lot of tasks.

In the buying phase, you’ll need:

After purchase, you’ll need:

It pays if all of this can be coordinated.

Some property agencies will do that for you. They’ll find you an investment-grade property, arrange the mortgage, the solicitors, the surveyor, and the insurance, find you tenants, manage the tenant relationship, organise maintenance and ensure you don’t fall foul of safety regulations.

The only jobs for you to do are speaking with your agent, signing any paperwork, and having the final say on any expenditures.

We now have such a service on MoneyUnshackled.com. Head over to the Find Me A Property page and send us a message using the form there if you want help buying and managing a rental property.

Our trusted property sourcer can find you the same kind of house that I myself invest in, following the same strategy outlined above of cashflow plus capital growth.

They’ll hold your hand through the buying process, discuss investment strategy with you, tailor a plan for your needs, and crack on with finding you that perfect opportunity.

Property is such a solid investment for 3 main reasons: the way it’s financed, the stability of the market, and the cash flow.

These investments work so well because you’re using an interest-only mortgage to buy your property with. If you had the incredible good fortune to be able to buy outright with cash, you’re ROI would plummet from 25%, to 9%.

A 9% return is still good, and is comparable to the stock market – but the property returns are only so high in our examples because I knew how to find a very good investment-grade property.

Most people wouldn’t know how to do that. That knowledge gap is why many landlords are being forced out of the market right now due to either making losses, or profits that are too small to justify the risk and effort. But regardless, financing a property right should magnify your returns.

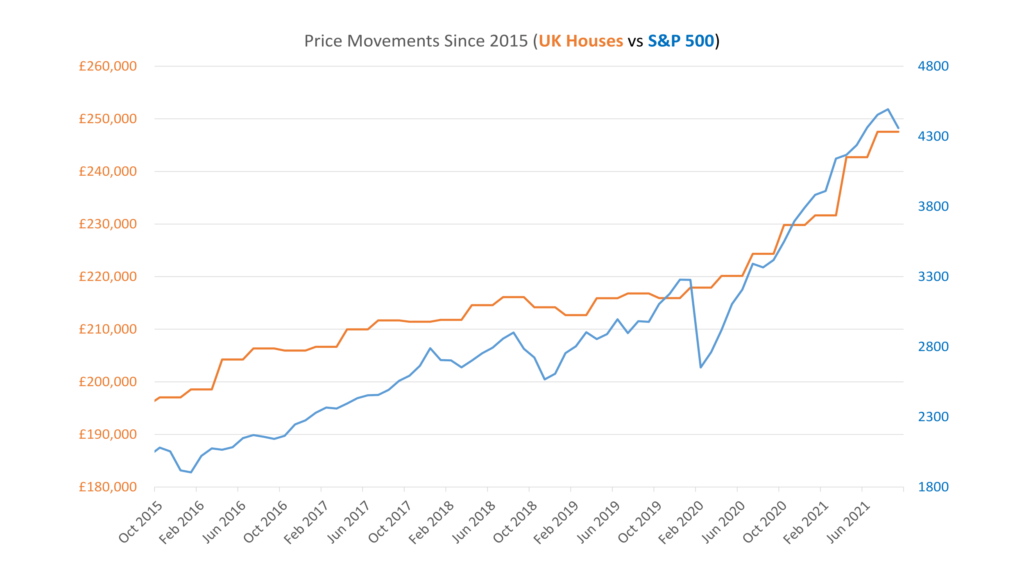

Historically, the property market has been extremely stable in comparison to the stock market, due to the nature of the asset – ordinary people need to live in them, and there’s always more demand than supply, so it’s very rare for prices to crash.

Above are the last several years for example – stock prices move wildly, while property moves much more smoothly. While price instability isn’t a major concern for a long-term strategy, a smooth gradual upward price journey can be reassuring to more risk-averse investors.

Finally, the properties we’re looking at here cash-flow very nicely, with over a third of the profits being cash in the bank as opposed to theoretical capital growth. You can spend that money on your lifestyle, or to replace a job income, or to easily reinvest into more assets.

The main downsides to buy-to-let are government meddling, tenant issues, and the large upfront investment amount required. Looming interest rate rises are also a common worry.

Let’s quickly deal with the first ones – keeping on top of ever-changing government regulation and tenant issues. These are both easily resolved by employing a property agent to run the day-to-day for you. Using a good property sourcer will also allow you to avoid buying a house in the first place that will need expensive renovations to meet upcoming law changes.

Off the top of my head, there’s a big one coming in 2030 that states that all rentals must have an energy rating of C or higher – not many older properties will be up to code without a fair bit of expenditure on insulation. The trick is in finding the good ones, or spending money smartly to improve the ratings just enough.

But the government comes up with new doozies like this all the time to keep landlords on their toes. Having someone on the end of the phone to advise you is invaluable.

Next, the upfront investment amount is typically a huge hurdle for most people. There are ways to effectively borrow more on your home residence to free up spare cash, called equity release that we’ve discussed previously, that a good mortgage broker will be able to help you arrange. Or you can go halves with a mate. Or you can even keep buy-to-let as an aspiration that you have on your radar until you’ve saved up enough.

That 25% we quoted for a passive investment was of course based on the current market, and a lot can change. But that doesn’t have to mean “change for the worse”.

Rents are skyrocketing right now, which is great for existing landlords, and helpful for new investors to the market as increasing rents offset the increases in property prices to maintain a high ROI. And if you jump into the market now, you can hopefully continue to ride the wave of rental price increases for years to come.

One big turd in the punchbowl though is interest rates. We don’t believe interest can rise all that much without every homeowner with a mortgage in the land being instantly bankrupted – not to mention the government’s own debt, who’s interest payments would rise by a painful £25bn a year for every 1% rise in interest rates.

The Bank Of England knows this, and will not want to take a course of action with interest rates that will sink the whole country.

Using the same logic as before, if rates rise by 1%, the 25% ROI drops to 23%. If we raise interest by 2%, ROI drops to 20%. If we raise interest by 3%, at which point the whole country is probably bankrupt, your ROI drops to 18%. The country may be screwed at this point, but you’re probably doing ok – thanks in part to the capital gains.

We think steady house price growth is still a reasonable expectation for the long-term going forwards. During the high-interest 1970s and 80s when the Bank of England base rate for interest peaked at 17%, house price growth was frequently in the double-digits. And in entirely different circumstances, in the 12 months to September 2021 houses have grown by 10%.

Finally, if you’re still not sold on outsourcing everything, think about the money you could make with the time saved from not having the second job of being an active landlord.

They say time is money, and if you’re saving hours a week, there’s other stuff you could be doing to increase your income beyond having a property administration job. Or you could just, you know… enjoy your free time!

What do you think about outsourcing everything to do with property? Join the conversation in the comments below!

Written by Ben

Featured image credit: ranjith ravindran/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

To many people the reason why you invest is blindingly obvious but if everyone knows, then why isn’t everyone doing it? Many people don’t realise how important investing is – and if you’re new to this channel you might be one of them. Others might simply be overwhelmed and don’t know how to begin despite wanting to.

Well, you’re in the right place. Today, we’re going back to basics with a complete beginner’s guide to investing. We’re covering:

If there’s anything that’s unclear, please let us know down below and we will do our best to help you out.

“If you don’t find a way to make money while you sleep, you will work until you die” – Warren Buffett. A very poetic and sombre thought but very true, nonetheless.

There are many different reasons why somebody might invest but generally most people invest with the intention to have their money make more money. Hopefully, one day you can invest enough so that you can stop trading your time for money through working a job and can retire. The more you invest and the better return you get, the sooner you can retire if you wish.

Maybe retirement is not even on your radar yet but we’re betting that you’d like to make more money, so you can buy more of the things you want, so in this case why not get your money working hard for you.

And if that’s not enough to convince you of the benefits of investing, then maybe this more depressing fact will. The annual inflation rate in the UK jumped to 3.2% in August 2021 and is set to continue climbing to a predicted 6%, so if you don’t invest you will be fighting a losing battle and your money will be constantly falling in value in real terms. Wealthy people have always invested, and you should too!

Unfortunately, short-term expectations about how much money you can make investing can often be totally unrealistic. You might have heard that someone made a killing investing in a particular stock or in Bitcoin, or whatever it might be, and was able to retire in their early twenties. The fact is that these success stories are few and far between – almost mythical.

Someone asked me whether it was worth investing as they’d seen you could start from £1 and someone they knew had made £1,000. It is indeed very easy to make £1,000 investing but it’s never going to happen from a single £1 investment.

The good news is that you could very realistically make £1,000 in a single year if you invest £10,000 or more. Over the last 30 years, the S&P 500 – which is the 500 largest US stocks – has returned 10.4% per year on average. For 19 of those 30 years the return exceeded 10% and 4 of those years exceeded 30%.

It’s really important to understand that your investment returns will almost certainly not be in a straight line. Some years will have devastating losses while others – as we have seen – will make you epic profits. Investing is a long-term game, and you’ve got to think of investing as a lifestyle choice and something you will do forever.

The other good news is that while peoples’ short-term expectations are unrealistic, you will probably underestimate how much money you can make in the long-term. With a 10.4% annual return over 30 years, just a single £10,000 investment would morph into over £193,000. You could very easily become a millionaire by investing if you decide you want to.

Broadly speaking you have 3 choices:

Before you choose your investment platform, which we’ll look at next, you should first choose what account types you want to use. These include Stocks and Shares ISAs, SIPPs, General Accounts, LISAs, and a few others. We think everyone should probably have a Stocks and Shares ISA, and a SIPP and here’s why.

A Stocks and Shares ISA is a tax efficient account that allows you to invest without paying some taxes such as capital gains tax, and some dividend taxes. Think of it as a wrapper that protects your investments from the taxman. You can sell your investments and access the money at any time, so this is likely to be your main investing account. You can only invest £20k a year as it stands right now, and you can only pay into one Stocks and Shares ISA each year.

Another popular account is a SIPP or self-invested personal pension. These are awesome for consolidating old workplace pensions into, give you enormous freedom in what you can invest in, and tend to be very low-cost. However, if you’re employed and saving into a pension you will likely want to prioritise your workplace pension as you get employer contributions with this, which you are unlikely to get with a SIPP.

As SIPPs are just a type of pension you won’t be able to access the money until age 55, and this is likely to rise in future.

With General accounts you have total freedom; you can open as many as you like and invest as much as you like. Any investment gains or dividends you earn though will be liable for tax.

A Lifetime ISA is an unusual account in that it’s used for either your first home or for retirement savings and has strict access limitations. If you are considering using a LISA we urge you to read our full LISA guide here.

Talking of guides, we have guides and best-buy tables for most of the stuff we’re talking about today, so check those out here.

If you’re a beginner we’re guessing you want to pay as little as possible in fees – at least until you have learned the ropes. The more expensive platforms tend to have better service and a bigger investment range, but you do pay for this.

We’ve got a thorough comparison of the best ISA platforms here, so head over there if you want to read up some more. For now though, let’s briefly look at a few of our favourite commission-free investing platforms that let you choose your own investments.

InvestEngine is currently our favourite. They offer a growing range of ETFs (more on what ETFs are in a moment) and they have zero charges. There are no set-up fees, no dealing fees, no account fees, and no foreign exchange fees. There are no fees from them whatsoever on the do-it-yourself side of the platform, which is awesome.

InvestEngine only offers ETFs, which we think is ideal for beginners because it keeps things super simple, and they’ve just added a feature that breaks your ETFs down by countries, sectors and companies, so you can see exactly what your portfolio is invested in.

We work closely with InvestEngine and new investors who use our link will get a £25 bonus when they deposit £100 or more (T&Cs Apply, capital at risk). Full details are listed on the MU Offers page, linked to here.

Our next favourite is Trading 212 but at time of filming they are closed to new investors. They will eventually be reopening but we don’t know when this will be. Trading 212 is almost free, but they do charge 0.15% in foreign exchange fees.

Trading 212 has an incredible range of stocks and ETFs considering it’s a commission-free app. But be careful which account you sign-up for; Trading 212 also offer CFDs – which is a type of derivative. We think beginners should avoid CFDs completely due to the high chance of losing all your money. As we already mentioned, an ISA is probably your best bet.

When they do reopen to new customers again, you’ll be able to get a free stock valued up to £100 with our special link (T&Cs Apply, capital at risk, full details on MU Offers page) – join the waitlist now and secure your free stock with this link.

Freetrade is another of our favourite commission-free apps. They too have a great selection of ETFs and stocks and have zero charges when you trade. However, out of the platforms we’ve mentioned in this video they do have the highest fees as they charge small amounts for an ISA account at £3 a month and have a larger foreign exchange fee at 0.45%.

New customers who use our link will get a free stock worth up to £200 (T&Cs Apply, capital at risk, full details on MU Offers page).

If you don’t want to invest for yourself and intend to use a robo-investing service instead, check out the written guide on robo-investing here.

In short, our favourite robo-investing platform is also InvestEngine, one reason being that they are the lowest priced at just 0.25%, which is insanely cheap compared to all the competition. FYI, they offer both a DIY service (which is free) and a robo-investing service (for a rock-bottom fee).

And Nutmeg, the market leader, has a competitively priced option at 0.45%, which is their ‘Fixed Allocation’ style. Welcome offers for both of these are also on the MU Offers page.

We’ve covered a lot of ground so far, but now you need to decide what to invest in and there’s a lot of noise everywhere leading unsuspecting noobies down the wrong path. Beginners often associate investing with buying Bitcoin, but cryptocurrency is pure speculation and highly volatile. It might be okay to speculate with a very small percentage of your money, but the bulk of your investments should be in funds containing global stocks and maybe some government bonds and gold.

Also, much of the excitement of investing comes from buying individual stocks and getting rich quick, and that is probably why many of the investing apps gamify investing. If you boot up an app like Freetrade or Trading 212, they place popular stocks and trendy themes in prominent positions within their apps. You can’t blame them because that is likely what most of their customers want.

Avoid the top movement tables and trends, avoid speculative punts on stocks, and avoid any investment which gives 3x exposure using leverage. And as a beginner avoid shorting, which aims to profit when something goes down. We think beginners should ignore all this noise and build a portfolio of ETFs that track global stocks. An ETF is simply a fund that holds a collection of securities such as stocks.

For example, the Vanguard FTSE All-World ETF (VWRL) invests in stocks from all around the world and contains almost 4,000 stocks including for example big names like Apple, Amazon, Nestle, and Toyota. An investor who builds a portfolio like this is placing their trust in the economic growth of the world’s biggest and best companies.

Our personal choice and what we invest in ourselves is what we call the Ultimate Portfolio, which contains just 5 carefully selected ETFs which have been chosen for their low cost, tax efficiency, and general awesomeness.

When investing in ETFs you can’t beat the website JustETF.com and the ETF provider’s own websites. JustETF.com has a free-to-use ETF screener that allows you to filter down so you can find ETFs in areas that you want to invest in. But before taking the plunge we always check out the ETF provider’s own site to examine further. Some of our favourite ETF providers are iShares, Vanguard and Invesco.

If you’re investing in individual stocks, you really need to analyse stock data and be able to screen stocks for good fundamentals. We use a site called Stockopedia, which is truly fantastic but it’s not cheap. Fortunately, we have arranged with them a 14-day free trial followed by a 25% discount for new customers through this link.

The best free site is Yahoo Finance but it’s worlds apart from the premium sites like Stockopedia!

Investing is risky and you could lose all your money but invest wisely across a diversified portfolio of ETFs and this is highly unlikely.

The largest crash for the US S&P 500 in modern times was the global financial crisis from 2007, which saw losses of 57%. Looking back to 1929, the Great Depression witnessed a crash of 86%, but a lot has changed since then with far better regulation of financial markets, so we doubt it could ever be this bad again.

If you invest in individual stocks, you could very likely see even bigger declines than what we just looked at and it’s a very big possibility that an individual stock might never recover. If you invest in a broad index fund such as an ETF tracking the world you have history on your side, which has seen valuations only ever increase in the long-term.

In terms of how safe your money is with your chosen platform, it should be protected by the Financial Services Compensation Scheme, which protects your investments up to £85,000 but do check. Your platform also has to segregate customer money from their own.

Note, that the FSCS doesn’t protect you against picking a dud stock but rather protects against platform failure.

There’s a lot more we want to cover but are conscious that it might be too much detail in a beginner’s guide. We hope you have found this guide useful and if you did get value consider subscribing to the email list here.

As a beginner investor, what were your biggest investment fears? Join the conversation in the comments below.

Written by Andy

Featured image credit: SkazovD/Shutterstock.com

Also check out the MoneyUnshackled YouTube channel, with new videos released every Wednesday and Saturday:

When it comes to your finances have you ever told yourself a little white lie to justify spending, going into debt, or simply not saving, or made excuses why you haven’t done something when you know you should have? In today’s post we’re looking at the 7 biggest money lies we all tell ourselves.

It doesn’t matter how good you are with money; we reckon everyone tells themselves these money lies to some extent. Let us know down in the comments if you’ve been telling these porkies to yourself. Now, let’s check it out…

With InvestEngine you can build a portfolio of fractional ETFs for FREE. No trading fees – no FX fees. And, new users to the platform will receive a £50 welcome bonus if you use this link. Read our full InvestEngine review here.

Some research done in the US from 2010 showed that people tend to feel happier the more money they make only up until the point that they earn about $75,000 a year.

Once your basic needs are met, more money will not make you any happier. The major issue we’ve identified with money and happiness studies is that they always seem to intertwine the concept of more money with more work.

This is the trap that we see so many professional managers up and down the land fall into. You’ve only got so much time, so giving away all of it to your employer in the pursuit of a little extra money is clearly going to have a negative effect on your happiness. If you’re not happy with £40,000, then you won’t be happy with £50,000.

Anecdotally, most people we speak to say they were at their happiest when they were in school and at university – times in their lives when they had little to no money.

Ben and I (MU cofounders) became mates at university and while there we had an awesome time, and in a single year we each must have lived on less than £10,000 a year to cover rent, bills, food and living costs. Lack of money certainly didn’t make us unhappy.

In the years following when we had to endure soul crushing work, our colleagues and managers couldn’t understand why we pursued shortened workweeks for less overall pay, when they and everyone else only ever wanted more and more money.

We think that once you earn £40,000 or more in the UK, then it’s not worth working longer hours to earn any more. At that point you need to think about earning more time to do things that interest you – new hobbies, spending time with family, rest and relaxation, or whatever you like.

Ideally what you want to do if possible is to break the link between your time and how much money you earn.

Most people know they need to either start saving or save more but they convince themselves that everything is ok – they will “start saving later”. Deep down they know that if they are unable to put a few quid aside now, how on earth will they do it in the future? Their financial life is likely to get harder – not easier.

Some people are living with their parents and literally have no bills and yet still haven’t saved a single penny.

People move on to have expensive kids of their own and buy bigger and bigger houses – you don’t see many 45-year-olds downsizing to 1 bed flats. Also, once you have become accustomed to a more expensive lifestyle it’s extremely difficult to go backwards, which you’ll likely need to do in order to start saving.

As we mentioned we loved our no-frills student lifestyle, but I could never go back to living like that. My expectation bar is now set way too high. Ignorance was bliss.

Just recently I’m annoyed that my new flat doesn’t have soft close toilet seats as that’s now what I’m used to. I know that sounds ridiculous when said out loud, but my standards have been raised. These won’t be that expensive to replace but it’s just one example of lifestyle creep that individually is so small that it’s barely noticeable. Now, multiply it across your entire life!

Most people are no different, so if you’re young start saving now before you raise your expectations, and if you’re a little older you may just have to bite the bullet, slash some expenses, and find a way to save now.

And if you’re still BSing yourself, saying that you don’t need to worry about retiring because you’re only in your twenties, you need to understand that money invested now is worth way more to your retirement than money invested later.

If a 20-year-old invests £100 a month for just 10 years and then stops contributing but allows the pot to continue growing until age 70, earning 8%, their final pot is worth £444k.